What is balance sheet?

Balance sheet refers to a financial statement which reveals the complete financial position of the company for a given date. A company’s balance sheet tells you the details of assets, liabilities and owners’ equity for the business. In simple words, the balance sheet is a statement which tells you the assets of the business, the money others need to pay you and the debt you owe others including the owner’s equity.

It answers three fundamental questions about your business:

- What do you own? (your assets — machinery, cash, stock, property)

- What do you owe others? (your liabilities — loans, unpaid bills, taxes)

- What is actually yours? (owner's equity — what remains after all debts are paid)

Balance sheet objectives

A balance sheet is also called as a top financial statement. Let’ us understand this by knowing the purpose and objective of the balance sheet. The following are some of the key objectives of the balance sheet:

- It helps in ascertaining the financial position of the business on a given day.

- Details of owner’s equity can be determined

- The information from the Balance sheet helps you create provision for future loss/contingencies by creating reserves

- It provides a snapshot of business health including the economic resources the business owns, owes, and the sources of financing for those resources.

- Ascertain if the business is financially autonomous and therefore solvent

- Determine the financial liquidity of the business

Features of Balance Sheet

- It provides a snapshot of a company's financial position at a specific point in time.

- It consists of assets, liabilities, and equity arranged according to the accounting equation Assets=Liabilities+Equity

- It helps assess liquidity, solvency, and capital structure.

- It displays reserves and surplus under equity, separating capital reserves and revenue reserves.

- It is prepared periodically and follows standardized accounting principles for consistency and comparability.

Balance Sheet Updates in India — FY 2024-25

Before we dive into the format, here are the key changes you must know:

1. New ICAI Format for Non-Corporate Entities (Effective from FY 2024–25)

The Institute of Chartered Accountants of India (ICAI) has introduced a new standardized balance sheet format applicable from 1st April 2024 onwards. This applies to:

- Sole proprietorships (individual shop owners, freelancers)

- Partnership firms

- HUFs (Hindu Undivided Families)

- Trusts, associations, and societies

What changed? The new format clearly separates current and non-current assets/liabilities, requires detailed disclosures on related party transactions, and classifies entities into four levels (Level I to IV) based on size and turnover — with different compliance requirements for each.

2. Schedule III Format for Companies

All companies registered under the Companies Act, 2013 must continue to prepare their balance sheets under Schedule III, which mandates a vertical format with equity and liabilities on top and assets below.

What are accounts receivable in Balance sheet?

Accounts receivable (also called debtors or trade receivables) is the money your customers owe you for goods or services you've already delivered — but haven't been paid for yet.

It appears on the Assets side of the balance sheet under Current Assets.

Example: You supply stationery to a school worth ₹50,000 in March but they pay you in April. Until they pay, that ₹50,000 is your accounts receivable.

Managing receivables well ensures you're not cash-starved even when your business is profitable on paper.

More on Accounts Receivables: Definition, Examples, Process and Importance

What are accounts payable in balance sheet?

Accounts payable (also called creditors or trade payables) is the money your business owes to its suppliers for goods or services received but not yet paid for.

It appears on the Liabilities side under Current Liabilities.

Example: You buy raw materials worth ₹1 lakh from a vendor in March with a 30-day payment period. Until you pay, it's accounts payable.

Keeping payables in check ensures you maintain good supplier relationships and avoid cash flow crunches.

Accounts payable is any sum of money owed by a business to its suppliers shown as a liability on a company's balance sheet. In simple words, when you buy goods or services with an arrangement to pay at a later date, such amount till it is paid is referred to as accounts payable.

Accounts payable is also called as bills payable and the total amount that a company is liable to pay is shown as liability under the head ‘sundry creditor’ in the balance sheet.

More on Accounts Payable – Definition, Example and Process

Reconciling balance sheet accounts

Balance sheet reconciliation means verifying that every entry in your balance sheet is accurate and supported by actual records. Reconciliation of balance sheet gives you a clear picture of your financial health and is also an indicator of all the entries being captured, accurately. Several businesses reconcile their balance sheet against their bank statements. You can also use your sub-ledgers, such as accounts receivables reports, accounts payables reports or even fixed asset transactions to ensure that your balance sheet is accurate.

Here's a simple approach:

- Match your bank balances against your bank statement

- Cross-check accounts receivable against your customer invoices

- Verify accounts payable against supplier bills

- Reconcile inventory with your stock register

What is a budgeted balance sheet?

A budgeted balance sheet is a future-looking version of your balance sheet. Instead of showing what happened, it forecasts what your balance sheet will look like at the end of a future period — if you stick to your current budget and business plans.

It helps business owners and CFOs:

- Plan for future cash needs

- Set targets for reducing liabilities

- Anticipate financial risks before they happen

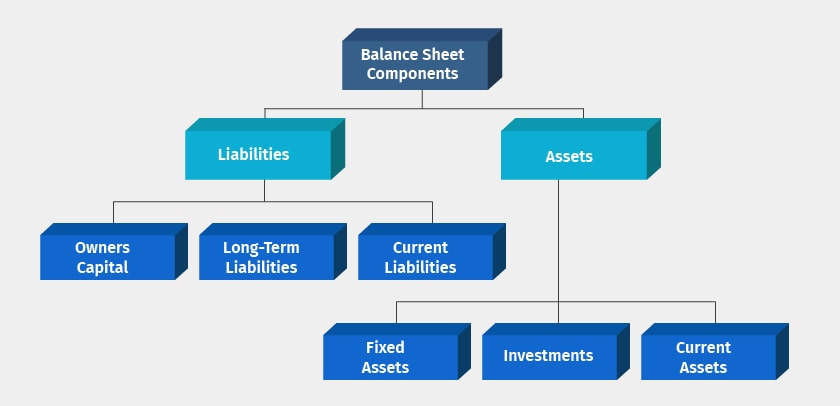

Balance sheet components

Balance sheet components are broadly divided into ‘Assets’ and ‘Liabilities’. Each of this balance sheet components consists of several sub-components. The following are balance sheet items:

[caption id="" align="alignnone" width="840"] balance sheet components[/caption]

balance sheet components[/caption]

As shown in the above balance sheet illustration, assets are broadly classified into fixed assets, investments and current assets. Similarly, liabilities are classified as owner’s capital, long-term debts and current liabilities. Let’s understand these balances sheet items in detail.

Assets (Everything Your Business Owns)

Something that an entity has acquired or purchased and owned, regarded as having value and available to meet debts, commitments or legacies. Assets are further broadly classified as:

Fixed Assets (things you keep for the long term) These are items your business uses for more than one year and doesn't plan to sell quickly:

- Land and buildings

- Machinery and equipment

- Vehicles

- Computers and furniture

- Patents and trademarks (called intangible assets — things you own but can't physically touch)

Current Assets (things that can become cash within 1 year)

Examples of current assets are, Cash, Bank balances, Investments, Deposits, Accounts receivables, and Inventory

Liabilities (Everything Your Business Owes)

A liability is any debt or obligation your business must repay. Liabilities are also split into two types:

Non-Current Liabilities (long-term debts — due after 1 year)

- Bank term loans

- Deferred tax liabilities

- Long-term borrowings from partners or investors

Current Liabilities (short-term debts — due within 1 year)

- Accounts payable / creditors — money you owe your suppliers

- Short-term bank loans / overdraft

- GST and income tax dues

- Salaries payable to employees

Owner's Equity / Shareholders' Funds — What Truly Belongs to You

Owner's equity is what remains after all liabilities are subtracted from assets. In simpler words — if you sold everything your business owns today and paid off all debts, this is what would be left for you.

It includes:

- Share capital — money invested by the owner or shareholders

- Reserves and surplus — accumulated profits kept in the business (not distributed as dividends)

What is Reserve in Balance Sheet?

A reserve in the balance sheet refers to a portion of a company's profits that is set aside or retained for a specific purpose or to strengthen the financial position. Reserves are a part of shareholders' equity and typically appear under "Reserves and Surplus" on the liabilities side of the balance sheet. Types of reserves:

- General Reserve — set aside for no specific purpose; acts as a safety buffer

- Capital Reserve — created from capital profits (e.g., profit on sale of assets)

- Specific Reserve — earmarked for a specific goal like expansion, debt repayment, or meeting future losses

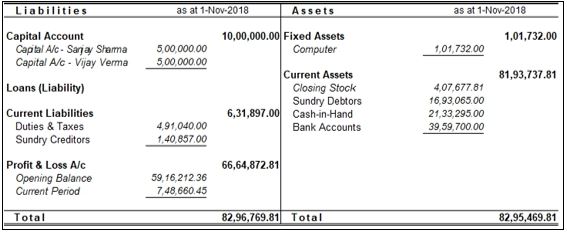

Balance sheet format

Below is the balance sheet format

[caption id="" align="alignnone" width="567"] balance sheet format[/caption]

balance sheet format[/caption]

As illustrated above, on the left side of the balance sheet format, all the assets are shown followed by the sub-components of assets. On the right side of the balance sheet format, liabilities followed with sub-components are displayed.

Balance sheet equations

As shown in the above balance sheet format, the balances of total liabilities and assets owned by the business always match. This implies that the total value of assets always adds up to the total liabilities of the business. The following are balance sheet equations:

- Assets = Liabilities + Owner’s Equity: This balance sheet equation tells you that all the assets owned by the business are either sponsored using the owners’ equity or the amount which company should owe others like suppliers or borrowings like loans

- Liabilities = Assets – Owner’s Equity: The difference of assets and owner’s investment into business is your liabilities which you owe others in the form of payables to suppliers, banks etc

- Owners’ Equity = Assets – Liabilities: This equation reveals the value of assets owned purely by owner equity

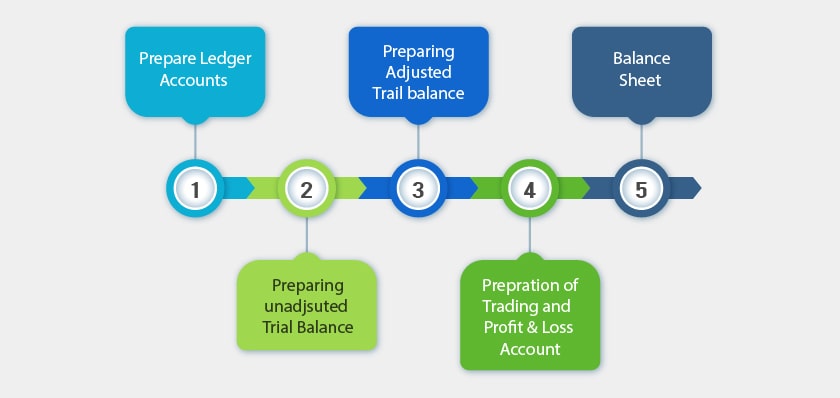

How to prepare a balance sheet?

Balance sheet preparation involves multiple steps to consolidate the accounting records and preparing various statements.

The following are the steps to prepare a balance sheet:

Here's the traditional process (don't worry — TallyPrime automates most of this):

- Record all transactions in your journal (daily entry book)

- Post entries to individual ledger accounts (grouped by type)

- Prepare a Trial Balance — a summary of all ledger closing balances

- Check that debit and credit totals match; fix any errors

- Prepare the Trading and Profit & Loss Account (income and expenses)

- Finally, prepare the Balance Sheet using remaining assets and liabilities from the trial balance

How TallyPrime makes balance sheet preparation effortless

If the above steps sound complex, that's because they can be — when done manually. That's exactly why thousands of Indian businesses use TallyPrime to handle it automatically.

With TallyPrime, you don't need to be an accountant to maintain accurate books. Here's what it does for you:

- Auto-generates your balance sheet the moment you enter transactions — no manual effort

- Comparative balance sheets — view side-by-side data across months, quarters, or years

- Branch-wise & consolidated balance sheets — perfect for businesses with multiple locations

- Schedule III compliant format — ready for audits and bank submissions right out of the box

- GST-integrated — your GST liabilities automatically reflect in the balance sheet

Balance sheet prepared by modern day business

Today, most businesses have automated balance sheet preparation using accounting software. Businesses believe using accounting software helps in saving time and efforts involved in managing books and preparing financial statements such as balance sheet. Further, the use of accounting software facilitates in generating comparative balance sheet – across periods and branches and consolidated balance sheet of all the branches or business verticals.

Watch Video on How to View and Analyse Balance Sheet in TallyPrime