The Profit and Loss (P&L) statement is a snapshot of a company's financial health over a specific period. It shows revenues, costs, and expenses in one place. This gives you a clear picture of a company's income, profits, and the costs incurred to earn those profits.

The main objective of a P&L statement is to show whether a company made a profit or lost money over a period, usually a month, quarter, or year. It does this by subtracting total expenses from total revenues.

This guide breaks the P&L statement into its parts and explains what each figure means. You'll learn how to read gross profit and net income margins, spot trends, and avoid common mistakes.

|

"Mastering the Profit and Loss statement unlocks the financial story of your business, and with tools like TallyPrime, you can navigate this narrative with precision and confidence." |

How to read Profit & Loss statement?

A Profit and Loss (P&L) statement can look complicated at first. But with the right approach, anyone can read it. Its structure and components are the key to understanding a company's financial performance.

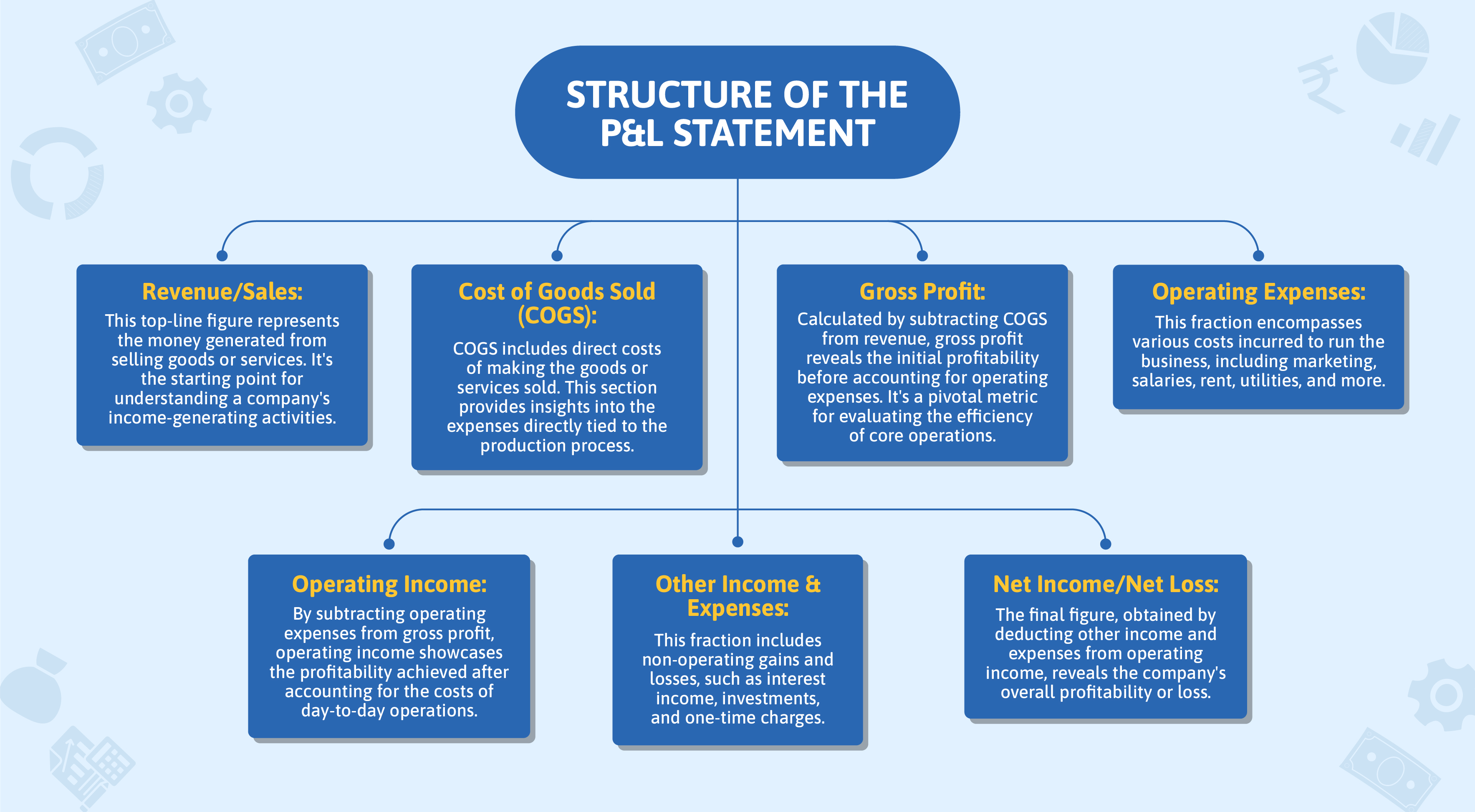

Structure of the Profit & Loss statement

A P&L statement is typically divided into a few sections. Together, they give a full picture of a company's financial activity for the period.

These sections include:

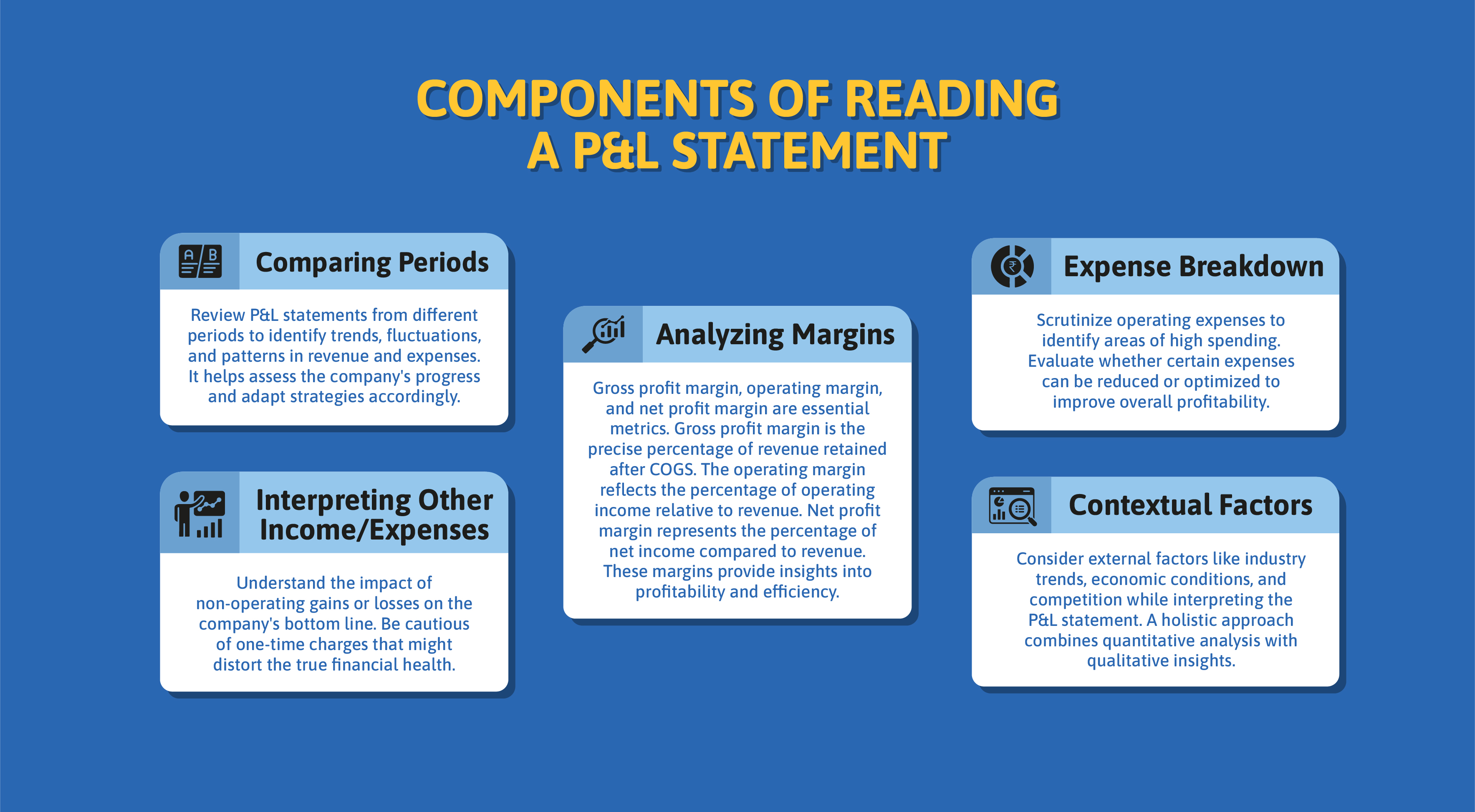

Components of reading a Profit & Loss statement

The P&L report is a key indicator of a business's success. It details the company's financial position and helps you understand its financial health.

Here are the important components for reading and interpreting a P&L report:

How to prepare a Profit and Loss statement?

Preparing a P&L statement has evolved. Today it blends traditional accounting practices with modern tools for speed and accuracy. Here's a look at both the traditional and modern-day approaches.

Traditional approach

Preparing a P&L statement traditionally meant entering financial data by hand into ledgers and journals. Accountants recorded revenues and expenses, cross-checking multiple documents for accuracy.

This method was slow and prone to human error. Data from different sources had to be collated and calculated manually to produce the final P&L statement.

Modern-day approach

Modern accounting software has changed the process. Businesses now use accounting software and financial management platforms to streamline P&L preparation.

These tools automate data entry, connect with other financial systems, and generate P&L statements in real time. Cloud-based solutions let stakeholders collaborate and access data from anywhere.

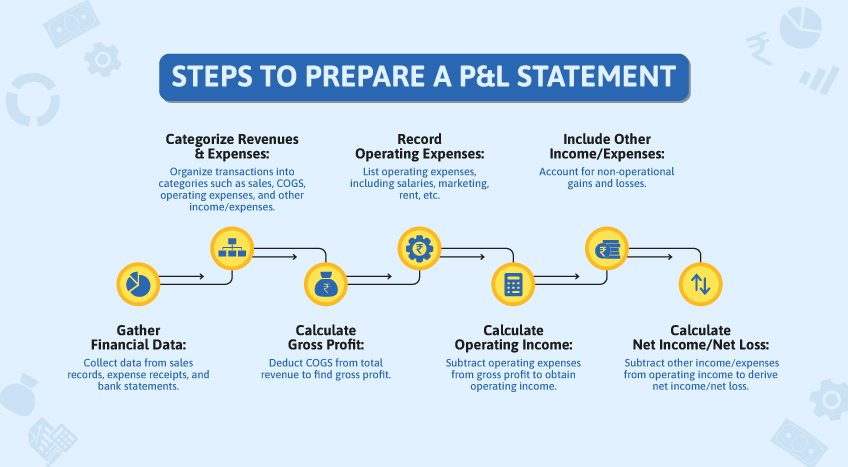

Steps to prepare a Profit & Loss statement

Preparing and analysing P&L in TallyPrime

TallyPrime streamlines preparing and analysing Profit and Loss (P&L) statements, giving businesses one platform for financial insights. Its user-friendly interface makes creating a P&L statement fast and accurate.

Preparing P&L in TallyPrime

- Data input: Easily input financial transactions, including revenue and expenses, through TallyPrime's intuitive data entry system.

- Automated categorisation: TallyPrime's intelligent algorithms automatically categorise transactions, reducing manual effort and ensuring accurate data organisation.

- Real-time calculations: TallyPrime performs real-time calculations as transactions are recorded, instantly updating the P&L statement as data is input.

Analysing P&L in TallyPrime

- Visual dashboards: TallyPrime offers visual dashboards that visually represent the P&L statement, aiding quick comprehension.

- Comparative analysis: Easily compare P&L statements across different periods to identify trends and make informed decisions.

- Instant insights: With TallyPrime's instant reporting capabilities, businesses gain quick insights into key metrics like gross profit margins and net income.

Wrapping up

A P&L statement is essential for steering a business toward success. Tools like TallyPrime bring efficiency and accuracy to modern financial management.

TallyPrime merges traditional accounting practices with modern technology to transform how you prepare and analyse P&L statements. Its interface simplifies data entry, automates categorisation, and delivers real-time calculations. Its visual dashboards and instant reporting give you a clear view of your business's financial health.

With TallyPrime, you can approach your company's financial data with confidence and make informed decisions that shape your business's direction.