What is Reverse Charge Mechanism (RCM) under GST?

RCM is a tax collection method where the recipient of goods or services is responsible for paying GST instead of the supplier. This mechanism is mandated by the GST Council to ensure tax compliance when the supplier is unregistered or when specific items are notified for reverse charge.

| Date | Update |

| 23rd July 2024 | The Union Budget 2024 proposed an amendment to Section 13 of the CGST Act. This amendment addresses the time of supply for services where the invoice is to be issued by the recipient in cases of reverse charge supplies from unregistered suppliers. This change will be effective upon notification by the CBIC. |

| 26th June 2024 | The Central Board of Indirect Taxes and Customs (CBIC) issued Circular No. 211/5/2024-GST, clarifying the recommendations by the GST Council regarding the availing of input tax credit under Section 16(4) of the CGST Act, specifically for cases where the recipient has issued the invoice under RCM. |

| 10th May 2023 | From 1 August 2023, e-invoicing became mandatory for taxpayers with an annual turnover exceeding ₹5 crore, impacting businesses that handle reverse charge transactions. |

RCM applies in two cases:

2. Unregistered suppliers: A registered business, when it buys from suppliers who haven't registered with the GST system, must pay GST under RCM.

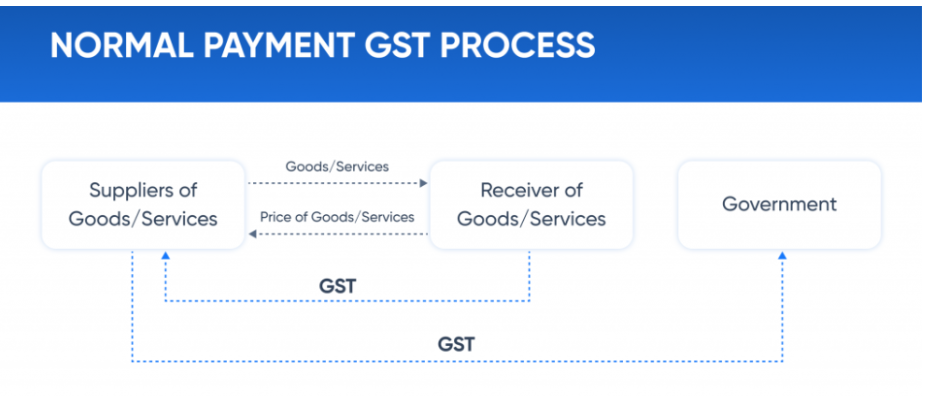

Normal GST Process :

Key definition (snippet‑ready)

Reverse Charge Mechanism (RCM): A GST provision in which the liability to pay tax rests with the buyer/receiver of a supply, rather than the seller.

Key Situations Where RCM is Applicable in GST

- Notified goods and services: Items listed in the GST Act (e.g., raw cotton, unprocessed cashew nuts, silk yarn, tobacco leaves).

- Unregistered suppliers: When a registered buyer purchases from a supplier who does not have a GST registration.

- Import of services: Services received from foreign vendors (e.g., SaaS platforms like Adobe Cloud) are taxed under RCM.

- Specific sectors: Construction services, real estate, and e‑commerce marketplace supplies are also covered.

Recent legislative updates (2024)

- Section 13 amendment (Union Budget 2024): Changes the time of supply for services where the recipient issues the invoice under RCM.

- CBIC Circular No. 211/5/2024‑GST: Clarifies eligibility of Input Tax Credit when the recipient issues the invoice.

- E‑invoicing mandate (effective 1 Aug 2023): Applies to businesses with turnover > ₹5 crore, impacting RCM transactions by requiring electronic invoice generation.

Step‑by‑step compliance guide for RCM

- Identify if the transaction falls under notified items or involves an unregistered supplier.

- Generate a Recipient Created Tax (RCT) invoice with GST details (taxable value, rate, amount).

- Pay GST to the government within the due date (usually the 20th of the following month).

- Claim Input Tax Credit in the same tax period, provided the supplier issues a valid invoice or a self‑invoice as per Circular 211/5/2024.

- Report the transaction in GSTR‑1 (as a reverse charge supply) and reflect the tax paid in GSTR‑3B.

Impact of RCM on businesses

RCM affects businesses in the following ways:

Cash flow impact: Since the recipient must pay GST upfront, it can impact working capital.

Accounting complications: Businesses need special systems to track their Recipient Created Tax (RCT) transactions.

Compliance obligations: The new system requires companies to maintain special records and manage their invoicing procedures.

Applicability of reverse charge with examples

Under RCM, all specified items must be subject to taxes regardless of supplier registration status.

1. Supply of notified goods and services

Certain goods and services are always taxed under RCM, regardless of whether the supplier is registered.

Examples of goods under RCM:

Raw cotton – Textile mills purchasing raw cotton from farmers must pay GST under RCM.

Cashew nuts (unprocessed) – Traders buying from farmers must pay GST.

Silk yarn – Manufacturers purchasing from unregistered suppliers must pay GST.

Tobacco leaves – Manufacturers must remit GST under RCM.

Examples of services under RCM:

Legal services – Businesses hiring independent advocates must pay GST.

Sponsorship services – Sponsors must bear the GST liability.

Goods Transport Agency (GTA) services – Companies using freight services must pay GST.

Director’s services to a company – GST is payable by the company.

2. Reverse Charge Mechanism on Import of Services in GST

Businesses must pay GST under the reverse charge mechanism when they buy services from non-Indian providers because foreign vendors do not have Indian GST registration. For example, an Indian IT firm using Adobe Cloud services (USA-based) must calculate and remit GST.

3. Reverse charge in e-commerce transactions

Under Section 9(5) of the CGST Act, the e-commerce operator must pay GST taxes for specified digital transactions on behalf of the service provider.

Some examples include the following:

Uber pays GST on behalf of its independent cab drivers.

Zomato pays GST on delivery services provided by restaurant partners.

4. Reverse charge in real estate & construction

RCM applies heavily in the construction sector, especially for subcontractors and works contracts. For example, a real estate company hiring an unregistered plumber must pay GST under RCM.

5. Security and manpower supply services

Security services or manpower supply from unregistered providers require the recipient to pay GST. For example, a corporate office hiring security guards from a small, unregistered agency must pay GST under RCM and generate a self-invoice.

6. Agricultural produce purchases

Since farmers are exempt from GST, businesses purchasing raw agricultural goods must pay GST under RCM. For instance, a food processing company buying raw wheat from farmers must pay GST under RCM.

List of Goods and Services Covered Under Reverse Charge Mechanism

Certain goods and services covered under RCM:

Goods under RCM

- Cashew nuts (unpeeled or unprocessed)

- Raw cotton

- Silk yarn

- Tobacco leaves

- Supply of lottery tickets

Services under RCM

- Legal services by an advocate

- Services by a director to a company

- GTA services

- Sponsorship services

- Import of services

Businesses must ensure to comply with RCM if they deal with these goods and services.

Time of supply for goods and services under reverse charge

Under GST, time of supply is crucial as it establishes when tax payment is due. The time of supply rules for goods and services under RCM differ from those in regular GST transactions.

Time of supply for goods under reverse charge

For goods purchased under RCM, the tax liability arises at the earliest of the following events:

Date of receipt of goods – The day the recipient physically receives the goods.

Date of payment – The day the recipient makes the payment to the supplier, whether in full or in part.

30 days from the date of the supplier’s invoice – If the invoice is issued but payment or receipt of goods has not occurred, tax liability still arises on the 31st day from the invoice date.

Time of supply for services under reverse charge

For services, the tax liability under RCM arises at the earliest of the:

Date of payment – The day the recipient makes the payment to the supplier.

60 Days from the date of the supplier’s invoice – If payment is not made within 60 days from the invoice date, tax liability is automatically triggered.

Input Tax Credit (ITC) under RCM

Businesses can claim ITC on GST paid under RCM, provided they have a valid tax invoice (or self‑invoice) and the supplier is not liable to collect tax. The credit is available in the same tax period as the payment, subject to the conditions laid down in Section 16(4) of the CGST Act.

Example of ITC under RCM

A company hires legal consultancy services from an advocate and pays 18% GST under RCM. The business can claim ITC for this amount in the same month when filing its GST return.

Correct recordkeeping of self-billed invoices allows companies to more effectively handle their GST claims and lower their total tax debt.

Who should pay GST under RCM?

The recipient of goods or services is liable to pay GST under RCM. This includes:

- Businesses purchasing from unregistered suppliers

- Service recipients availing notified services like legal consultancy

- Importers of goods and services

Reverse charge exemptions

Some exemptions exist under RCM:

- Goods or services below a specified value threshold

- Supplies from unregistered dealers if below ₹5,000 per day

- Certain government services exempted from RCM

For example, purchases from small unregistered suppliers may not attract RCM if they fall within exemption limits.

E‑invoicing and RCM

From 1 Aug 2023, entities with turnover > ₹5 crore must generate e‑invoices for all outward supplies, including RCM transactions. The e‑invoice must contain the reverseCharge flag set to “Y”. This ensures seamless integration with GSTN’s portal and automatic tax credit eligibility.

Common mistakes and penalties

- Failing to pay GST on time – attracts interest at 18% per annum and a penalty of up to ₹10,000.

- Not issuing a proper RCT invoice – leads to denial of ITC and possible prosecution.

- Incorrect reporting in GSTR‑1/GSTR‑3B – can trigger notices from CBIC.

How Tally helps you manage RCM

TallyPrime/Tally ERP 9 offers built‑in features to automate RCM compliance:

- Automatic generation of Recipient Created Tax invoices.

- Separate ledger for “RCM Payable” to track tax liability.

- One‑click ITC claim for reverse charge entries.

- Export-ready data for GSTR‑1 and GSTR‑3B filing.

Mandatory Registration for Reverse Charge Tax Payers

As per the GST rules, a taxable person who is liable to pay tax under the reverse charge mechanism, will need to take mandatory registration under GST , irrespective of turnover.

Conclusion

Understanding and correctly implementing the Reverse Charge Mechanism is crucial for GST compliance, cash‑flow management, and maximizing Input Tax Credit. Stay updated with the latest amendments, leverage e‑invoicing, and use Tally’s automation features to simplify RCM handling.

Read More on GST

GST Software, GST Software for CAs, GST Software for Traders, GST Invoicing Software, GST Calculator, GST on Freight, GST on Ecommerce, GST Impact on TCS, GST Impact on TDS, GST Exempted Goods & Services, GST Declaration

GST Rates & Charges

GST Rates, GST Rate Finder, GST Rate on Labour Charges, HSN Codes, SAC Codes, GST State Codes

Types of GST

CGST, SGST, IGST, UTGST, Difference between CGST, SGST & IGST

GST Returns

GST Returns, Types of GST Returns, New GST Returns & Forms, Sahaj GST Returns, Sugam GST Returns, GSTR 1, GSTR 2, GSTR 3B, GSTR 4, GSTR 5, GSTR 5A, GSTR 6, GSTR 7, GSTR 8, GSTR 9, GSTR 10, GSTR 11