E-invoicing under the Goods and Services Tax (GST) regime has revolutionized the way businesses manage their invoicing processes. It is a system that mandates the generation of invoices in a standardized electronic format, ensuring compliance and reducing errors. As of now, e-invoicing has become mandatory for businesses with an annual turnover exceeding ₹10 crores, making it essential for these entities to understand the e-invoice format to comply with GST regulations effectively.

In 2024, updates to e-invoicing regulations may include adjustments to turnover thresholds or changes in compliance requirements, emphasizing the need for businesses to stay informed about the latest developments.

What is E-Invoice in GST? - Meaning, IRN & How It Works

e-Invoice known as ‘Electronic invoicing’ is a system in which all B2B invoices are electronically uploaded and authenticated by the designated portal. It adheres to a specific format prescribed by the GST authorities.

| Best e-Invoicing Software Solution for Businesses in India | Generate e-Invoice Instantly in TallyPrime |

It plays a crucial role in the GST ecosystem by facilitating seamless data exchange between suppliers and tax authorities. E-invoicing integrates with the Invoice Registration Portal (IRP), where each e-invoice is assigned a unique Invoice Reference Number (IRN). Additionally, a QR code is generated, which contains essential details about the invoice, ensuring easy verification by tax authorities.

Know more on IRN, Format, and process to generate it.

Why is E-Invoicing Important for GST Filers? Benefits & Compliance Impact

E-invoicing is important for GST filers because it standardises invoice reporting, automates compliance, and sharply reduces errors and fraud in the GST system.

- Fewer errors and easier returns

Standard, IRP-validated e-invoices auto-populate GST returns and e-way bills, cutting manual data entry, mismatches, and reconciliation effort for filers. - Better ITC and cash flow

Real-time visibility of invoices speeds up input tax credit matching and reduces ITC disputes, which supports smoother cash flow for both suppliers and recipients. - Stronger compliance and transparency

Each e-invoice gets a unique IRN and QR code, making fake or duplicate invoices difficult and improving audit trails and tax compliance under GST.

E-Invoice Applicability - Who Must Generate E-Invoices Under GST?

Businesses required to generate e-invoices under GST are those whose aggregate annual turnover exceeds ₹5 crore (effective from August 1, 2023). The threshold initially started higher (₹100 crore in 2020) and has been progressively lowered to expand compliance across more businesses. This applies mainly to B2B sales as part of India's mandate to digitize and authenticate invoices through the Invoice Registration Portal (IRP). Aggregate turnover includes turnover across all GSTINs under a single PAN, so even if a single establishment's turnover is below ₹5 crore but the total exceeds this, e-invoicing is mandatory. Certain categories such as SEZ units, banks, and insurance companies may be exempted as per government notifications.

| Turnover Threshold | Effective Date |

|---|---|

| > ₹500 crore | 1 Oct 2020 |

| > ₹100 crore | 1 Jan 2021 |

| > ₹50 crore | 1 Apr 2021 |

| > ₹20 crore | 1 Apr 2022 |

| > ₹10 crore | 1 Oct 2022 |

| > ₹5 crore | 1 Aug 2023 |

The thresholds are subject to change; stay updated with GST notifications.

Key Components of an E-Invoice - 30 Mandatory Fields Explained

The mandatory fields of an e-invoice under GST (India) include the following key details:

- Supplier details: GSTIN, legal name, address

- Invoice details: Invoice number, invoice date, invoice type

- Buyer details: GSTIN (for B2B), legal name, address

- Place of supply (State code)

- Item details: Description, HSN code, quantity, unit, taxable value

- Tax details: GST rate, CGST/SGST/IGST amount

- Total invoice value

- IRN (Invoice Reference Number) – generated by IRP

- QR code – auto-generated with IRN

The following are the 30 mandatory fields of an e-invoice. Earlier, 50 fields were to be mandatorily filled by the taxpayer.

|

Field name |

Description |

|

Document Type Code |

Every type of document has a code and this must be specified in this portion. |

|

Supplier Legal Name |

The name of the supplier according to the PAN card details. |

|

Supplier GSTIN |

The supplier GSTIN for e-invoice. |

|

Supplier Address |

The full address of the supplier including flat number, building no. etc. |

|

Supplier Place |

The city/village/town of the supplier must be specified here. |

|

Supplier State Code |

The state must be selected. |

|

Supplier Pincode |

The six-digit PIN code of the supplier’s address. |

|

Document Number |

A unique invoice number that makes sense to the business. It has to be sequential for easy identification. |

|

Preceding Invoice Reference and Date |

The original invoice details are being edited using a document such as a credit note. |

|

Document Date |

The date on which the invoice was issued. |

|

Recipient Legal Name |

The name of the buyer is specified as per his PAN card. |

|

Recipient’s GSTIN |

The buyer’s GSTIN needs to be specified. |

|

Recipient’s Address |

The detailed address of the buyer has to be specified. |

|

Recipient’s State Code |

The place of supply has to be specified. |

|

Place of Supply State Code |

The state of the recipient has to be selected. |

|

Pincode |

The location of the recipient has to be selected. |

|

Recipient Place |

The village/town/city of the recipient has to be specified. |

|

Invoice Reference Number or IRN |

The supplier leaves the field empty at the time of registration, and after that, GSTIN generates a unique number when the e-invoice is uploaded on the GSTN portal. As the e-invoice is accepted, acknowledgment is sent. Before the use of an e-invoice, the IRN has to be displayed on it. |

|

Shipping To GSTIN |

GSTIN of the person the item is being delivered to. |

|

Shipping To State, Pincode and State Code |

This field specifies the place where the goods and services are delivered. |

|

Dispatch From Name, Address, Place, and Pincode |

The name of the dispatching entity, along with the city/town/village specifics. |

|

Is Service |

If the supply of service has to be specified. |

|

Supply Type Code |

The type of supply and its responding code is specified. It can be supplied to SEZ, B2B, etc. |

|

Item Description |

The item’s description. |

|

HSN Code |

The particular code for the goods or services. |

|

Item Price |

The GST exclusive unit price prior to the item price discount being subtracted. This value must be positive. |

|

Assessable Value |

The item’s price excluding GST and after the item price discount has been subtracted. |

|

GST Rate |

The rate of the specific item for which the invoice has been generated. |

|

IGST Value, CGST Value and SGST Value Separately |

Every item must have IGST, SGST, and CGST. |

|

Total Invoice Value |

The total value, including GST. |

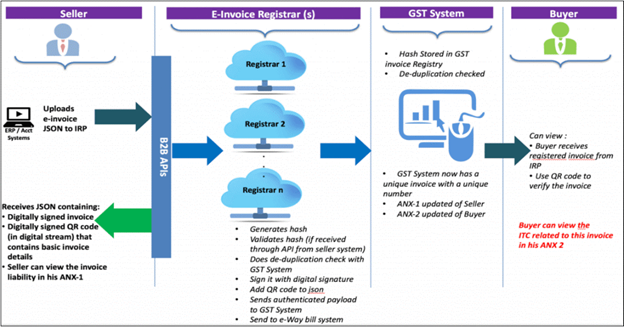

How Does E-Invoicing Work? — Step-by-Step Process on IRP

Step 1 – Generation of e-invoice:

The taxpayer will continue to generate invoices in the normal course of business. However, the reporting of these invoices electronically has criteria. It needs to be done as per the e-invoice schema, along with mandatory parameters. The mandatory fields of an invoice for the supply of goods are listed below:

-

- Invoice type

- Code for invoice type

- Invoice Number

- Invoice Date

- Supplier details like Name, GSTIN of Supplier, and Supplier address (including place, pin code, and state)

- Details of the buyer, such as name, GSTIN number, state code, address, place, pin code, payee name, account number, payment mode, and IFSC code

- Dispatch details

- Invoice item being dispatched

- Total tax amount paid amount, and payment due

- Tax scheme (whether GST, Excise Custom, VAT)

- ‘Shipping To’ details like Name, GSTIN, address, pin code, state, supply type, and transaction mode (whether regular, ‘bill to’ or ‘ship to’)

- Details of goods like Sl. no., quantity, rate, assessable value, GST rate, amount of CGST/SGST/IGST, total invoice value, batch number/name

The seller has to ensure that his accounting/billing software is capable of generating a JSON of the final invoice. The seller can create a JSON following the e-invoice schema and mandatory parameters by using the following modes:

-

- Accounting and billing system that offers this service

- Utility to interact with either accounting/billing system, ERP, excel/word document, or a mobile app

- Offline Tool to generate e-invoice by keying-in invoice data

Step 2 – Generation of unique IRN:

The supplier has the option to generate a ‘hash’ based on specific parameters, usually three of them, such as Supplier’s GSTIN, Supplier’s invoice number, Financial Year (YYYY-YY). The prescribed algorithm, such as SHA256 must be used for the hash generation. If the hash is validated, it will later become the Invoice Reference Number (IRN) of the e-invoice.

Step 3 – Uploading the JSON:

The following modes may be used to upload the JSON of the final invoice:

-

- Directly on the IRP

- Through GST Suvidha Provider (GSP)

- Third-party provided apps (including through API)

- The supplier can also upload the hash along with the JSON onto the IRP if generated by him

Step 4 – Hash generation/validation:

The hash will have to be generated by the IRP in respect of the invoices uploaded without the hash. In such a case, the hash generated by the IRP would become the IRN. Where the supplier has also uploaded the hash, a de-duplication check will be performed. It is done by validating the hash/IRN against the Central Registry of the GST System to ensure that the IRN is unique. Once validated, the hash/IRN is stored in the Central Registry. IRP will then generate a QR Code and digitally sign the invoice and make it available to the supplier. The IRP also sends the e-invoice via e-mail mentioned on the invoice to the buyer and seller.

Time Limit to Generate E-Invoice - 7-Day IRP Rule Explained

The time limit to generate an e-invoice under GST depends on the date of invoice:

- An e-invoice must be generated within 7 days from the invoice date on the IRP

- This rule applies to eligible taxpayers covered under e-invoicing

- E-invoices generated after 7 days are rejected by the IRP

Example:

If the invoice date is 1st April, the e-invoice must be generated on or before 7th April.

- Benefits of E-Invoicing Under GST - For Businesses & Tax Compliance

The basic aim behind the adoption of the e-invoice system is to pre-populate the returns and reduce the reconciliation challenges. This is achieved by the design of the IRP system which shares the invoice data to the GST system and e-way bill system. Thus, continuous uploading of invoices will ensure that most of the details required in returns as well in the e-way bill get auto-populated.

The following are some of the key benefits of e-invoicing:

- Reduces reporting of same invoice details multiple times in different forms. It’s just a one-time upload and everything, as required, will get pre-populated.

- Part-A of e-Way bill will be auto-captured and only transporter details are required to be updated.

- On uploading of invoices, the B2B details will be auto-captured in GSTR-1 return.

- Substantial reduction in input credit verification challenges as the same data will get reported to the tax department as well to the buyer in his inward supply (purchase) register (GSTR-2A).

- On receipt of info from the GST System, a buyer can do a reconciliation with his Purchase register and accept/reject it on time under New Return.

- A complete trail of B2B invoices and system-level matching of input credit and output tax helps to reduce tax evasion.

- Increase efficiency in tax administration by eliminating fake invoices.

E-Invoice Compliance Requirements Under GST — Rules & Notifications

E-invoicing is mandatory for GST-registered entities whose gross annual turnover exceeds ₹5 crore in any financial year since 2017-18. The rule came into effect on August 1, 2023. The change has been made through Notice No. 10/2023 – Indian Taxation System, which intends to boost compliance and facilitate the digitalization of business transactions.

Time Limit to Generate E-Invoice

For businesses with Annual Aggregate Turnover (AATO) of ₹10 crore or more, every e-invoice (including debit/credit notes) must be reported on the IRP within 30 days from the invoice date, effective 1 April 2025.

If the invoice is uploaded after 30 days, the IRP rejects it, meaning no IRN/QR code is generated and the document becomes invalid for GST compliance and ITC purposes.

E-Invoicing vs Manual Invoicing - Before & After Comparison

Before e-invoicing

- Invoices created manually or in separate systems

- Data entered multiple times (accounting, GST portal, e-way bill)

- Higher risk of errors and mismatches

- Delayed reporting and reconciliation

- Limited real-time visibility for tax authorities

After e-invoicing

- Invoices generated digitally in accounting software

- Auto-reporting to IRP with IRN and QR code

- Single data entry used for GST returns and e-way bills

- Fewer errors and faster reconciliation

- Real-time compliance and better transparency

E-Invoice Turnover Limit - Current Threshold, History & Exemptions

Current Threshold

- Threshold Limit: Entities whose annual gross revenue exceeds ₹5 crore require the generation of e-invoices for all B2B transactions.

- Previous Threshold: Previously, before the amendment in August 2023, the threshold was set at ₹10 crore.

Applicability

E-invoicing would be required for all GST-registered businesses whose turnover exceeded ₹5 crore in any financial year during the period from 2017-18 to date.

Aggregate turnover growth means the total revenues across all GSTINs under one PAN in India.

Exemptions

Certain services may be exempt from e-invoicing requirements, e.g.

- Small taxpayers below the threshold limit.

- Specific sectors or types specified by the government.

How TallyPrime Supports E‑Invoicing

- Built‑in IRP integration – Direct API connection eliminates manual uploads.

- Automatic IRN retrieval– TallyPrime fetches and embeds IRN/QR in real time.

- Auto‑populate GST returns– Exported data feeds GSTR‑1 and GSTR‑2A without extra effort.

- Error‑free validation – Pre‑submission checks flag missing mandatory fields.

- Scalable for large volumes– Handles bulk invoice generation for enterprises.

Read Articles

- How to Generate e-Invoice in GST?

- Generate e-Invoice Instantly in TallyPrime

- Bulk Generation of e-Invoices in TallyPrime

- How does e-Invoice System Work

- How to amend or modify e-invoices?

- How to Transit to e-Invoice System?

- Things to consider while choosing an e-invoice solution

Watch How to Set-up TallyPrime for e-invoice

Video guide - e-invoicing in TallyPrime

Know more about e-invoices in GST