- TDS on purchase of goods under section 194Q

- Scenarios of TDS deduction u/s 194Q

- Steps to manage TDS on purchase u/s 194Q in TallyPrime

In India, businesses are required to deduct TDS (Tax Deducted at Source) on certain payments like interest, salary, rent, and professional fees. However, from 1st July 2021, a new rule has been added under Section 194Q of the Income Tax Act. This section makes it mandatory for buyers to deduct TDS when purchasing goods if the purchase value crosses a certain limit. The main aim of this rule is to keep a better track of large transactions and improve tax compliance. It’s especially relevant for businesses with high turnover or those involved in bulk buying.

In this guide, you’ll learn when Section 194Q applies, how to calculate TDS and key exceptions.

Applicability of Section 194Q

Section 194Q applies only under certain conditions. It is important to check whether these conditions are met before deducting TDS on the purchase of goods.

Who needs to deduct TDS under Section 194Q?

You must deduct TDS under Section 194Q if:

- Your business turnover was more than ₹10 crore in the previous financial year.

For example, if you are checking for the financial year 2024–25, your turnover in 2023–24 must have been above ₹10 crore. - You are purchasing goods worth more than ₹50 lakh from a single seller during the current financial year.

If both of these conditions are true, you are required to deduct TDS on the amount that exceeds ₹50 lakh.

Calculation of TDS under Section 194Q

Once you're required to deduct TDS under Section 194Q, the next step is to calculate it correctly. The TDS is not on the full value of the purchase, but only on the portion that exceeds ₹50 lakh from a single seller in a financial year.

Calculation Method:

Use the following formula:

TDS Amount = (Total Purchase Value – ₹50,00,000) × TDS Rate

Where:

- TDS Rate = 0.1% (if PAN is available)

- TDS Rate = 5% (if PAN is not available)

Example:

If your purchases from a seller total ₹80 lakh during the year, then:

- Amount liable for TDS = ₹80 lakh – ₹50 lakh = ₹30 lakh

- TDS (assuming PAN is available) = ₹30,00,000 × 0.1% = ₹3,000

This amount must be deducted from the payment and deposited with the government.

Scenarios of TDS deduction u/s 194Q

|

Details in a financial year |

Use Case-1 |

Use-case-2 |

Usecase-3 |

Use case-4 (PAN not Available) |

|

Turnover of Buyer |

15 Cr |

20 Cr |

8 Cr |

14 Cr |

|

Sale Value or consideration |

60 Lakhs |

8 Lakhs |

20 Lakhs |

70 Lakhs |

|

TDS deduction by buyer |

Yes |

No |

NO |

Yes |

|

Taxable value |

10 Lakhs |

-- |

-- |

20 Lakhs |

|

Rate of TDS |

0.1% |

-- |

-- |

5% |

*Taxable value refers to the value more than 50 lakhs i.e., the remaining amount of purchase after 50 lakhs. In cases where the buyer is not eligible to deduct TDS, the seller can collect tax on meeting threshold criteria.

Steps to manage TDS on purchase u/s 194Q in TallyPrime

For ease of recording TDS on purchases u/s 194Q in TallyPrime, follow the steps mentioned below. To know step-by-step by details to configure and recording translations, please read Record TDS on Purchase of Goods (Under Section 194Q)

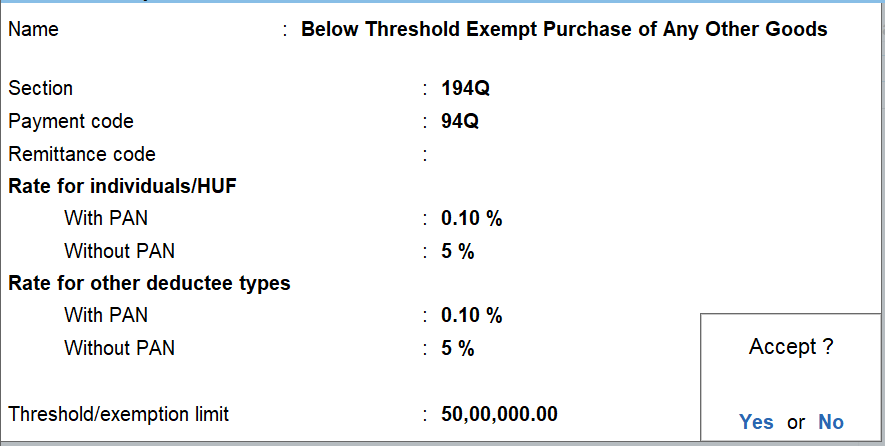

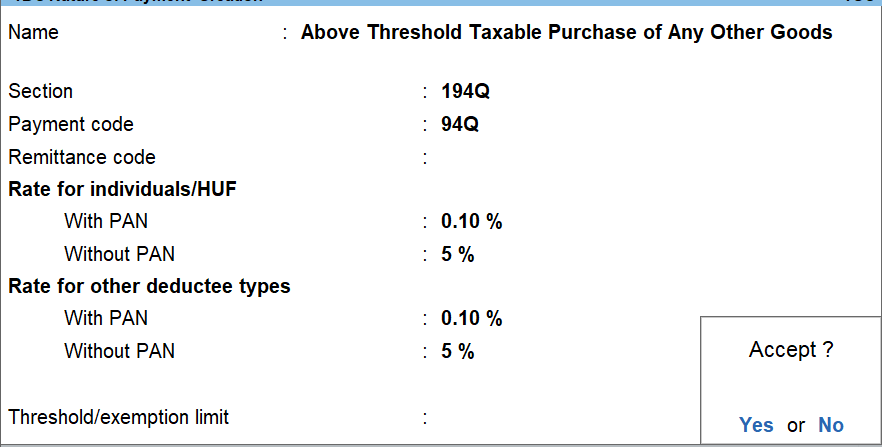

Creation of TDS nature of payment

Create two ‘TDS Nature of Payments’ and configure one above the Threshold Limit (of Rs 50 lakhs) and one below the limit as shown in the images below. You can name the nature of payment accordingly for easy identification. Also, mention the rate as 0.10% with PAN and 5% in case of without PAN.

To create, navigate from Gateway of Tally > Create > type or select TDS Nature of Payments. Alternatively, press Alt+G (Go To) > Create Master > type or select TDS Nature of Payments.

Purchase ledger and GST ledgers configuration

Configure the purchase ledger and GST ledgers to ensure that both GST and TDS is applicable, and set the TDS Nature of Payment to ‘Any’.

Recording transactions

While recording the purchase transaction, you have to select the relevant nature of payment in the ‘TDS Nature of Payment’ details sub-screen.

- If the total value of purchases from a party crosses the Threshold Limit across transactions, you have to select the nature of payment configured above the Threshold Limit

- if the total value of purchases from a party continues to be below the Threshold Limit, you have to select the nature of payment configured below the Threshold Limit

Read Record TDS on Purchase of Goods (Under Section 194Q) to know more on managing advance TDS payment, adjust TDS in purchase as per advance payment, purchase return/cancellation and TDS exemption for government-listed seller

Exceptions and Exemptions

Although Section 194Q applies to many buyers, there are some situations where this rule does not apply. Knowing these exceptions helps avoid unnecessary confusion and ensures compliance only when required.

|

Exception |

Explanation |

|

Turnover is below ₹10 crore |

Buyer is not required to deduct TDS |

|

Seller is a non-resident |

Section 194Q applies only to purchases from resident sellers |

|

TDS is already applicable under another section |

Example: Section 194-O (E-commerce transactions) |

|

TCS under Section 206C(1H) applicable and buyer not liable under 194Q |

Seller may collect TCS if the buyer is not required to deduct TDS |

Compliance and Penalties

When you deduct TDS under Section 194Q, it’s important to follow all the compliance rules carefully to avoid penalties.

What you need to do to comply:

- Deduct TDS on time: You must deduct TDS when making the payment or crediting the amount to the seller, whichever happens first.

- Deposit TDS with the government: The deducted TDS amount should be deposited with the government within the prescribed time.

- File TDS returns: You must file TDS returns regularly, providing details of TDS deducted and paid.

- Provide TDS certificate: You need to issue a TDS certificate (Form 16A) to the seller as proof of tax deducted.

Penalties for non-compliance:

- Disallowance of expense (Section 40A(IA)): If you fail to deduct TDS under Section 194Q, 30% of the purchase amount on which TDS was not deducted will not be allowed as a business expense.

This means:- That 30% will be added to your taxable income

- You will need to pay tax on it as part of your total income

- Prosecution in serious cases: In cases of wilful failure, legal action may be taken, including fines and imprisonment.

Following these rules ensures you stay compliant and avoid unnecessary fines or legal trouble.

FAQ

Who should deduct TDS u/s 194Q?

You should deduct TDS under provision 194Q if the annual turnover of your business exceeds Rs 10 crore in the previous financial year.

What types of purchases you need to deduct TDS u/s 194Q?

You need to deduct TDS if you purchase goods worth more than Rs 50 lakhs from a single vendor in the same financial year. Apart from this, there are other conditions such as purchases should be from a resident and TDS has not been deducted under any other provisions of the Income Tax Act

What is the time or point at which TDS needs to be deducted?

TDS is required to be deducted at the time of credit of such sum to the account of the seller or at the time of payment whichever is earlier. In other words, if you are making payments to the party or while booking the purchase invoice, whichever is earlier, you have to deduct TDS and pay the remainder of the amount to the seller.

What is the rate of TDS?

You need to deduct TDS at 0.1% if the seller has a PAN, or at 5%, if the seller does not have a PAN.

Is TCS applicable if TDS is deductible by the buyer of the goods?

No. Section 194Q clarifies that if a buyer is liable to deduct TDS on a purchase transaction, the seller shall not collect TCS on the same transaction.