GST (Goods and Services Tax) is a unified, destination-based indirect tax implemented in India to replace multiple central and state taxes. In 2026, GST follows a rationalized 3-tier structure (5%, 18%, and 40%), focusing on digitized compliance and real-time ITC validation to simplify the 'Ease of Doing Business' for MSMEs.

India's tax landscape changed permanently on July 1, 2017. With a single stroke, over 17 different central and state taxes — each with its own rates, forms, deadlines, and interpretations — were replaced by one unified framework: the Goods and Services Tax, or GST.

This guide is written for people who actually run businesses — not for tax officers. We'll cover everything from first principles to what most businesses still get wrong in 2026.

What is GST in India?

GST stands for Goods and Services Tax. It is a comprehensive, indirect tax levied on the supply of goods and services across India. The term 'indirect' means the tax is not paid directly to the government by the consumer — it is collected by the seller at the point of sale and then remitted to the government.

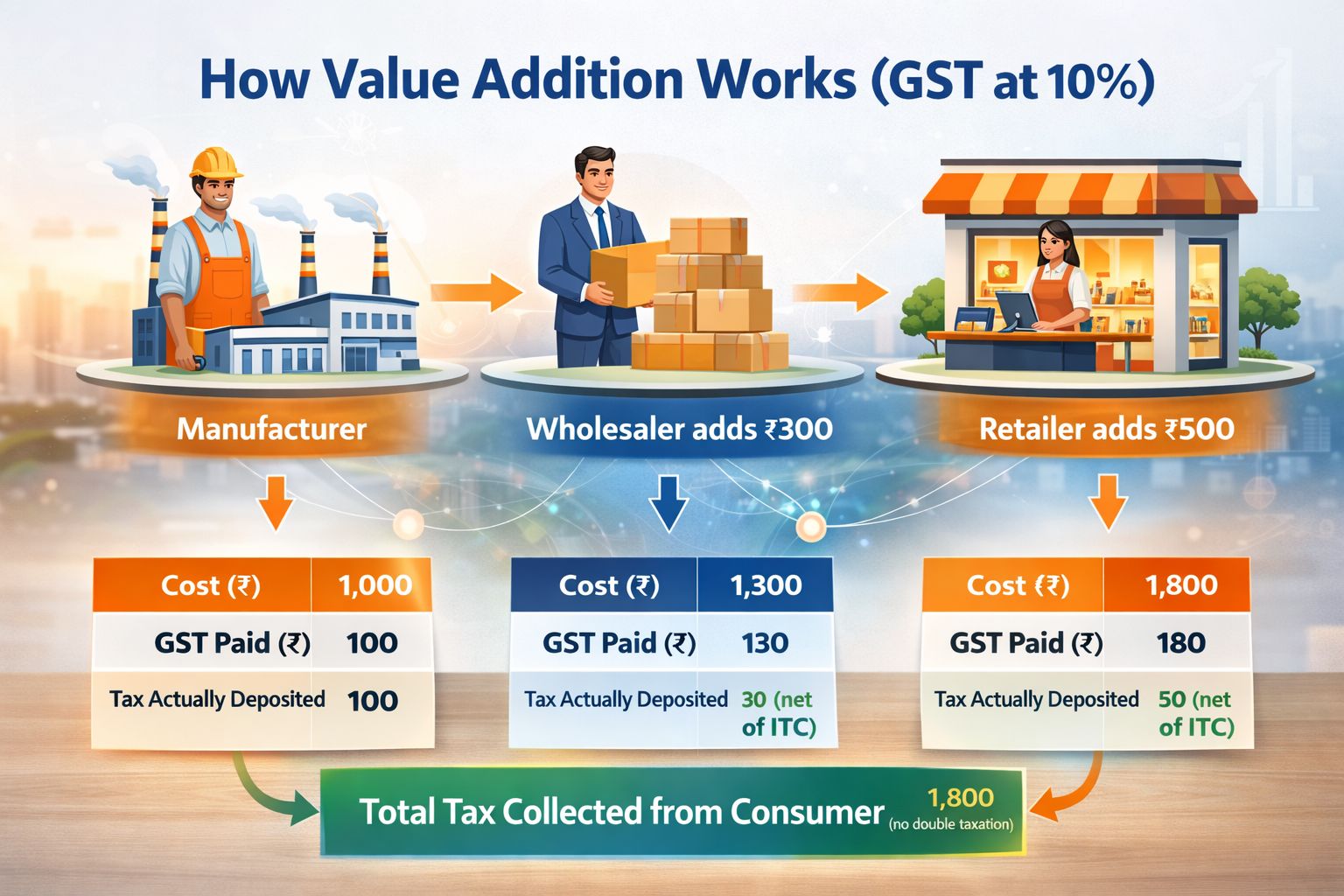

What makes GST unique among indirect taxes is its design. Unlike the earlier system, where multiple taxes were stacked on top of each other (leading to what economists call the 'cascading effect'), GST allows each business in the supply chain to claim credit for the tax paid at the previous stage. You only pay tax on the value you add — not on value that has already been taxed.

The Three Defining Characteristics of GST

1. Multi-Stage

GST is not a one-time tax. It is collected at every stage of a product's journey — from raw material sourcing, to manufacturing, to warehousing, to retail, and finally to the end consumer. At each stage, the business pays GST on its purchases and collects GST on its sales. The difference between what it collects and what it paid becomes its tax liability for the period.

2. Destination-Based

Under GST, the tax revenue goes to the state where the goods or services are consumed — not where they are produced. This was a fundamental shift from the previous regime, where producing states had significant tax advantages.

For example, if a factory in Gujarat manufactures goods and sells them to a consumer in Karnataka, the entire GST revenue goes to Karnataka — the state of consumption. This made the GST a fairer revenue-sharing mechanism for consuming states.

3. Value Addition-Based

GST is levied only on the value added at each stage of production or distribution — not on the total value of the product. This is what eliminates the cascading effect and keeps prices lower for the end consumer.

The Journey of GST in India — 25 Years in the Making

GST did not happen overnight. It was the result of two and a half decades of political debate, economic modeling, constitutional amendments, and negotiation between the Centre and 29 states. Understanding its journey explains why it is designed the way it is.

|

Year |

Milestone |

|

2000 |

Prime Minister Vajpayee sets up the first committee to design a GST framework for India. |

|

2006 |

Finance Minister P. Chidambaram announces a target date of April 1, 2010 for GST implementation. |

|

2008 |

The Empowered Committee of State Finance Ministers finalises the dual GST model — keeping both Centre and States as independent taxing authorities. |

|

2011 |

The Constitution Amendment Bill for GST is introduced in Parliament but lapses due to political opposition. |

|

2014 |

The new NDA government reintroduces the GST Bill in Parliament. Momentum builds across party lines. |

|

2016 |

The Constitution (101st Amendment) Act is passed, paving the way for GST. The GST Council is constituted. GSTIN infrastructure goes live. |

|

Mar 2017 |

Four supplementary GST Acts (CGST, IGST, UTGST, Compensation) are passed in Parliament. |

|

Jul 1, 2017 |

GST officially launches at the midnight stroke of the clock in the Central Hall of Parliament — a moment described as India's most significant tax reform since Independence. |

What took 17 years? The core challenge was political: GST required states to surrender their right to levy their own taxes on goods. In return, they would receive their share of a combined revenue pool — but the distribution formula was contested for years. The eventual breakthrough came with a constitutional guarantee: the Centre would compensate states for any revenue shortfall during the first five years of GST. That promise broke the deadlock.

The India Before GST — Why the Old System Was Broken

To truly appreciate GST, you need to understand what it replaced. The pre-2017 tax system wasn't just complicated — it was structurally contradictory. It created a situation where the same product was taxed multiple times by different authorities, using different rates, with different compliance requirements — and no mechanism to offset one against the other.

The Cascading Effect: A ₹1,000 Problem

Here's a concrete example. Before GST, a textile manufacturer in Maharashtra buying cotton would pay:

- Central Excise Duty on the manufacture of fabric

- VAT charged by the state on the sale of fabric to a dealer

- CST (Central Sales Tax) if the fabric crossed state lines

- Entry Tax when goods entered certain states or municipal limits

- Octroi in some cities, a local tax on goods entering city limits

The dealer buying that fabric could not offset the Central Excise Duty paid by the manufacturer against the VAT they owed — because they were administered by different authorities under different laws. The result: tax on tax. Every rupee of tax paid at an earlier stage became part of the cost base on which the next tax was calculated.

|

Taxes Subsumed by GST |

Taxes Still Present After GST |

|

Central Excise Duty |

Basic Customs Duty |

|

Service Tax |

Tax on Petrol, Diesel & ATF |

|

Value Added Tax (VAT) |

Tax on Tobacco & Alcohol |

|

Central Sales Tax (CST) |

Stamp Duty on Property |

|

Luxury Tax |

Electricity Duty |

|

Entertainment Tax |

Vehicle Tax |

|

Entry Tax / Octroi |

Property Tax |

|

Advertisement Tax |

|

|

Taxes on Lotteries & Betting |

|

Note: Petroleum products (crude, diesel, petrol, natural gas, aviation turbine fuel) and alcohol for human consumption remain outside GST's scope — they continue to attract state and central levies separately. This is one of the most discussed unfinished items on India's tax reform agenda.

The Three Components of GST — CGST, SGST, and IGST

India adopted a dual GST model — meaning both the Centre and States have the right to levy GST on the same transaction simultaneously. This was the political compromise that made GST possible. In practice, it works through three types of GST:

CGST — Central Goods and Services Tax

Levied by the Central Government on transactions that happen within a single state (intra-state). If you buy goods and the supplier is in the same state, CGST is one of the two taxes applied. The revenue goes entirely to the Central Government.

SGST / UTGST — State / Union Territory GST

Levied by the State Government (or Union Territory administration) on the same intra-state transaction. The revenue goes to the state. CGST and SGST are always equal — if the GST rate is 18%, it's 9% CGST + 9% SGST.

IGST — Integrated Goods and Services Tax

Levied by the Centre on inter-state transactions — when goods or services move from one state to another. The Centre collects the revenue and then distributes the state's share to the destination state (not the origin state — reflecting GST's destination-based character). IGST rate is approximately the sum of CGST + SGST rates.

|

Type of Transaction |

Tax Applied |

Who Collects |

Revenue Goes To |

|

Sale within the same state (e.g., Mumbai to Pune) |

CGST + SGST |

Centre + State |

Split equally between Centre & State |

|

Sale across states (e.g., Delhi to Chennai) |

IGST |

Centre |

Centre distributes state share to destination state |

|

Import into India |

IGST + Customs |

Centre |

Centre (Customs) + destination state (IGST share) |

GST Rates in India — What Falls Where

GST in India operates on a multi-slab rate structure, designed to apply lower taxes on essentials and higher taxes on luxury or sin goods. The primary GST rate slabs are:

|

Rate |

What It Covers |

|

0% (Nil) |

Essential goods and services: fresh fruits and vegetables, milk, curd, bread, salt, unbranded grains, educational services, health services from clinical establishments, and services by RBI/SEBI. |

|

5% |

Mass consumption items: packaged food, cooking oil, sugar, tea, coffee (not from cafes), domestic LPG, e-books, transport services (railways, air travel economy class), restaurant services (non-AC). |

|

18% |

Air conditioners, televisions, refrigerators, Small cars (≤1200cc petrol/≤1500cc diesel), Entry-level bikes (≤350cc), Cement, auto parts, buses, trucks, ambulances, Apparel above ₹2,500 |

|

40% |

Luxury and demerit goods: cars, motorcycles above 350cc, cigarettes and tobacco, Carbonated & caffeinated beverages |

|

Special rates |

3% on gold, silver and jewellery. 5% on making charges 0.25% on rough, precious stones. |

The Composition Scheme — A Simpler Option for Small Businesses

Businesses with annual turnover below ₹1.5 crore (₹75 lakh for certain states) can opt for the Composition Scheme. Under this scheme:

- They pay GST at a flat, reduced rate (1% for traders, 5% for restaurants, 6% for service providers)

- They cannot charge GST on their invoices or collect it from customers

- They file quarterly returns instead of monthly ones

- They cannot claim Input Tax Credit

The Composition Scheme is ideal for small local businesses with minimal interstate trade. However, it is not suitable for businesses that supply to GST-registered buyers — because those buyers will not receive any ITC from a Composition dealer.

Input Tax Credit (ITC) — The Most Powerful (and Most Misused) GST Feature

Input Tax Credit is the mechanism that makes GST non-cascading. It allows a registered business to deduct the GST paid on purchases from the GST collected on sales. Only the net amount (output tax minus input tax) is paid to the government.

ITC is arguably the most significant feature of GST for businesses — but also the one with the most compliance pitfalls. Getting ITC wrong can result in unexpected tax demands, interest payments, and penalties.

How ITC Works — A Simple Example

Assume a furniture manufacturer operates in Rajasthan:

- Buys wood (raw material) from a local supplier for ₹50,000 + GST at 12% = ₹6,000 GST paid

- Sells finished furniture to a Jaipur dealer for ₹80,000 + GST at 12% = ₹9,600 GST collected

- Net GST liability = ₹9,600 − ₹6,000 = ₹3,600 payable to the government

Without ITC, the manufacturer would pay ₹9,600 in GST on top of the ₹6,000 they already paid on purchases — effectively taxing their inputs twice. ITC eliminates this double burden.

GST Registration — When You Need It and How to Get It

Not every business in India needs to register for GST. Registration becomes mandatory once you cross certain turnover thresholds — or when you engage in specific types of supply that require GST registration regardless of turnover.

Registration Thresholds

|

Category |

Threshold (Most States) |

Threshold (Special Category States*) |

|

Supplier of Goods |

₹40 lakh |

₹20 lakh |

|

Supplier of Services |

₹20 lakh |

₹10 lakh |

|

Supplier of Both Goods & Services |

₹20 lakh |

₹10 lakh |

*Special Category States include Manipur, Mizoram, Nagaland, Tripura, Meghalaya, Sikkim, Arunachal Pradesh, and Uttarakhand.

When Registration Is Mandatory Regardless of Turnover

Certain businesses must register for GST even if their turnover is below the threshold:

- Businesses making inter-state supply of goods

- Casual taxable persons (those who supply goods or services occasionally in a state where they have no fixed place of business)

- Non-resident taxable persons

- E-commerce operators and suppliers selling through e-commerce platforms

- Persons required to deduct TDS under GST

- Input Service Distributors

- Persons supplying on behalf of other taxable persons (agents)

How to Register: Step by Step

- Visit gst.gov.in and click 'New Registration.'

- Fill Form GST REG-01 with business details, PAN, Aadhaar, bank account details, and address.

- Upload required documents: PAN card, Aadhaar card, proof of business address, bank statement or cancelled cheque, and a photograph of the proprietor/authorised signatory.

- Complete Aadhaar authentication or opt for in-person verification.

- The GST officer reviews the application. If documents are in order, GSTIN is issued within 3–7 working days.

GST Returns — What You Must File and When

Filing GST returns is an ongoing compliance obligation for every registered taxpayer. Unlike income tax, which is filed annually, GST returns are filed monthly, quarterly, or annually depending on the type and size of your business. Missing deadlines attracts interest at 18% per annum and late fees that accumulate daily.

|

Return |

Purpose |

Who Files |

Frequency / Due Date |

|

Details of outward supplies (sales invoices) |

All regular taxpayers |

Monthly by 11th; Quarterly (QRMP) by 13th |

|

|

Summary of sales, ITC claimed, and tax paid |

All regular taxpayers |

Monthly by 20th; Quarterly by 22nd/24th |

|

|

Auto-populated ITC statement (read only — not filed by taxpayer) |

Auto-generated for buyers |

Available on 14th of following month |

|

|

Annual return for Composition Scheme dealers |

Composition taxpayers |

Annual, by 30th April |

|

|

Annual return reconciling the full year's GST filings |

Regular taxpayers (turnover > ₹2 crore) |

Annual, by 31st December |

|

|

GSTR-9C |

Reconciliation statement certified by CA/CMA |

Taxpayers with turnover > ₹5 crore |

Annual, with GSTR-9 |

|

TDS deducted under GST |

TDS deductors |

Monthly by 10th |

The QRMP Scheme — Quarterly Filing for Smaller Businesses

The Quarterly Return Monthly Payment (QRMP) scheme allows taxpayers with annual turnover up to ₹5 crore to file GSTR-1 and GSTR-3B quarterly instead of monthly. However, tax payments must still be made monthly (by the 25th) either by self-assessment or using a fixed sum (35% of tax paid in the last quarter). This reduces the compliance burden from 24 returns per year to just 8.

New compliance under GST -E-Invoicing and E-Way Bills

Two digital compliance requirements underpin the modern GST system: e-invoicing for B2B transactions and e-Way Bills for the movement of goods. Both were introduced after GST's launch and have significantly strengthened the system's ability to detect tax evasion.

E-Invoicing — What It Is and Who It Applies To

E-invoicing (or electronic invoicing) does not mean creating an invoice on a computer. It means getting your B2B invoice validated and registered on the government's Invoice Registration Portal (IRP) before it is sent to your buyer.

Here's how it works:

- Your accounting software generates an invoice.

- The invoice is uploaded to the IRP in a standard JSON format.

- The IRP validates the invoice and assigns it a unique Invoice Reference Number (IRN) and digitally signs it with a QR code.

- Only after receiving this IRN is the invoice considered a valid GST invoice for ITC purposes.

|

Annual Turnover Threshold |

E-Invoicing Mandatory From |

|

Above ₹500 crore |

October 1, 2020 |

|

Above ₹100 crore |

January 1, 2021 |

|

Above ₹50 crore |

April 1, 2021 |

|

Above ₹20 crore |

April 1, 2022 |

|

Above ₹10 crore |

October 1, 2022 |

|

Above ₹5 crore |

August 1, 2023 |

E-Way Bills — For Moving Goods

An e-Way Bill is an electronic document required for the movement of goods valued above ₹50,000. It must be generated on the e-Way Bill portal before the goods are dispatched.

Key facts:

- Required for inter-state movement of goods valued above ₹50,000

- Required for intra-state movement in most states (check your state's specific rules)

- Generated by the supplier, the recipient, or the transporter — whoever moves the goods first

- Contains details of the supplier, recipient, goods, vehicle, and route

- Valid for a distance-based period (1 day per 200 km for normal cargo; 1 day per 20 km for oversized cargo)

Transporting goods without a valid e-Way Bill invites detention of goods, a penalty equal to 100% of the tax due (or 200% for exempted goods), and in repeat cases, confiscation.

GST Eight Years On — The Real Impact on Indian Businesses

It's easy to read about GST's benefits in policy documents. But eight years of implementation have produced a more nuanced reality — one with genuine wins and persistent friction points. Here is an honest assessment.

Where GST Has Delivered

1. Logistics Has Transformed

Pre-GST, trucks would wait for hours — sometimes days — at state border checkposts to pay octroi and state entry taxes, and to get documentation stamped. The elimination of these checkposts after GST is estimated to have reduced average transit times by 20–30% on major national routes. This is not a policy claim — it's visible in logistics company data and in the reduction of inventory held at warehouses near state borders.

2. The Tax Base Has Widened Dramatically

In 2017, India had approximately 65 lakh (6.5 million) indirect tax registrations. By 2025, GST has over 1.45 crore (14.5 million) active registrations. This near-doubling of the tax base has brought a large segment of the informal economy into the formal system — businesses that previously transacted in cash with no tax trail now need GSTIN-backed invoices to participate in B2B commerce.

3. Revenue Has Consistently Grown

Monthly GST collections have grown from an average of ₹90,000 crore in 2017–18 to consistently crossing ₹1.7–1.8 lakh crore in 2024–25. This growth represents both economic expansion and improved compliance — a direct result of e-invoicing, return matching, and real-time data analytics by the GSTN.

Where Friction Persists

1. ITC Reconciliation Remains a Headache

Despite the introduction of GSTR-2B as a matched statement, the reality for many businesses — especially those with hundreds of suppliers — is that mismatches between GSTR-2B and purchase ledgers are common. Suppliers file late, amend invoices, or report incorrect amounts. Each mismatch requires follow-up, documentation, and sometimes deferral of ITC claims. For large businesses, this is a monthly exercise that consumes significant accounting bandwidth.

2. Rate Classification Disputes

India's GST rate structure, with five primary slabs and numerous exemptions and exceptions, creates genuine classification ambiguity. Is a fortified fruit drink taxed at 12% or 28%? Does a specific type of construction service attract 5% or 18%? These questions have generated thousands of advance rulings, court cases, and assessments — many of which are contradictory across states. Small businesses, without access to specialist GST counsel, often err in classification — sometimes in their own favour, sometimes against.

3. Return Complexity for Multi-State Businesses

A business operating in five states files GSTR-1, GSTR-3B, GSTR-9, and potentially GSTR-9C for each state registration — every year. That's potentially 20+ returns annually, each requiring reconciled data. The government has simplified some processes (QRMP scheme, auto-population), but multi-state compliance remains resource-intensive for SMBs without dedicated tax teams.

10 GST Mistakes Businesses Make — and How to Avoid Them

These are the errors that actually show up in GST assessments, audit reports, and demand notices. If you recognise your business in any of these, act before the department does.

- Claiming ITC Without Verifying Supplier GSTIN Status. The most common and most costly mistake. Before recording a purchase invoice, check that the supplier's GSTIN is active, and that they are filing their returns. Use the GSTIN verification tool to confirm status. A cancelled or suspended GSTIN means your ITC claim will be rejected.

- Incorrectly Classifying Goods or Services Under the Wrong HSN/SAC Code. Wrong HSN codes lead to wrong rates, wrong ITC claims, and mismatches in GSTR-1. The government's systems flag rate inconsistencies across the supply chain. Always use the official HSN code lookup tool and confirm with your CA for any product where you're uncertain.

- Missing the ITC Claim Window. ITC for FY 2024–25 must be claimed by November 30, 2025. Many businesses discover unclaimed ITC during annual return preparation — only to find the window has closed. Monitor your purchase register against GSTR-2B monthly.

- Claiming ITC on Blocked Credit Items. Buying a car for director use, catering for an office party, or insuring a company vehicle — these are blocked credits under Section 17(5). Many businesses claim them, and many get caught during assessments. Maintain a clear list of blocked credit categories and train your accounts team.

- Not Generating e-Way Bills for All Qualifying Movements. Some businesses generate e-Way Bills only for inter-state movements, missing the intra-state requirement. Others forget that goods sent for job work, goods returned by customers, or goods dispatched for exhibition also require e-Way Bills above the value threshold.

- Filing GSTR-3B Without Reconciling Against GSTR-2B. Filing GSTR-3B by copying last month's numbers, or estimating ITC without checking GSTR-2B, is a shortcut that creates long-term compliance risk. Every rupee of ITC claimed in 3B should be traceable to a specific invoice in GSTR-2B.

- Not Reversing ITC When Supplier Payment is Overdue. If you do not pay a supplier within 180 days of the invoice date, you are required to reverse the ITC claimed on that invoice, along with interest. Many businesses are unaware of this rule. Set up payment tracking linked to your GST compliance calendar.

- Applying the Wrong GSTIN on Inter-State Invoices. A business with multiple state registrations must use the GSTIN of the state from which the supply is being made. Using the wrong GSTIN turns an inter-state supply into a seemingly intra-state one — misrepresenting the tax to the wrong state government.

- Ignoring GST Notices. The GST department sends notices through the portal — not by post. Many businesses never check their GST portal dashboard and miss notices for mismatches, non-filing, and pending responses. Ignoring a GST notice does not make it go away — it triggers assessment proceedings and ex-parte orders.

- Not Maintaining Invoice-Level Documentation. GST audits require you to produce the original tax invoice, proof of receipt of goods/services, and proof of payment for every ITC claim. Maintaining only summary-level records is insufficient. Digitise and archive all purchase invoices with their corresponding GSTINs

GSTIN — The Identity Number at the Heart of GST Compliance

Every registered taxpayer under GST is assigned a GSTIN — Goods and Services Tax Identification Number. It is a 15-character alphanumeric code that serves as the taxpayer's permanent identity in the GST system. Understanding its structure is useful for quickly spotting errors or potential fraud.

Decoding the 15 Characters of a GSTIN

|

Characters |

What It Represents |

Example / Notes |

|

1–2 |

State Code |

29 = Karnataka, 27 = Maharashtra, 07 = Delhi. A mismatch between the state code and the supplier's claimed location is a red flag. |

|

3–12 |

PAN of Taxpayer |

The 10-character PAN. This directly links the GST registration to the taxpayer's income tax identity. Verify this against the PAN shown on the invoice. |

|

13 |

Entity Number |

1, 2, 3... if the same PAN has multiple registrations in the same state. Most businesses show '1'. |

|

14 |

Default 'Z' |

Always 'Z' in current registrations. Any other character here is a structural error. |

|

15 |

Check Code |

An algorithmically generated digit/letter for error detection. Cannot be guessed — a fabricated GSTIN will often fail here. |

Why Verifying a GSTIN Before Every Transaction Matters

A GSTIN that was active when you onboarded a supplier may be cancelled six months later — due to non-filing, malpractice, or a department order. Transacting with a cancelled GSTIN and claiming ITC on those invoices exposes you to tax demand, interest, and penalties.

Best practice: verify GSTINs at three stages:

- On vendor onboarding: Before adding a new supplier to your purchase ledger.

- Before issuing a purchase order: Especially for high-value transactions.

- Before processing payment on large invoices: A cancelled GSTIN discovered after payment is an expensive problem.

GST State Codes — The First Two Digits That Matter Most

Every GSTIN begins with a two-digit state code. These codes are not arbitrary — they are the same codes used by the Census of India and the Indian vehicle registration system. Understanding GST state codes is important for three practical reasons: verifying that a supplier's GSTIN matches their claimed location, ensuring your inter-state invoices carry the correct IGST treatment, and detecting structurally invalid GSTINs.

How State Codes Affect Your GST Compliance

Intra-State vs Inter-State — the Tax Treatment Depends on Codes

When the state code in the supplier's GSTIN matches the state code in the buyer's GSTIN, it is an intra-state supply — CGST and SGST apply. When they differ, it is an inter-state supply — IGST applies. Your accounting software determines this automatically when both GSTINs are entered correctly. But if a GSTIN is entered incorrectly — or manually overridden — the wrong tax is applied, creating a mismatch between your filing and your counterparty's.

State Code Mismatches — A Common Red Flag for Fake GSTINs

When verifying a vendor's GSTIN, cross-check the first two digits against the state they claim to operate from. A supplier who presents an invoice from a Mumbai address but whose GSTIN starts with '29' (Karnataka) has either:

- A legitimate second registration in Karnataka (possible — ask for both GSTINs), or

- Used a GSTIN belonging to a different business, or fabricated the number entirely

Neither scenario should be dismissed without explanation. A quick call to the vendor and a search on the GSTN portal resolves it in minutes. Ignoring the mismatch costs far more later.

Multiple State Codes for the Same Business

A business operating in multiple states will have a different GSTIN for each state — each with its own state code. A national distributor with warehouses in Delhi, Mumbai, Chennai, and Kolkata will have four GSTINs starting with 07, 27, 33, and 19 respectively — all with the same PAN in positions 3–12. This is entirely normal and expected.

Special Category States and Their Compliance Implications

States with codes 01 (J&K), 02 (Himachal Pradesh), 05 (Uttarakhand), 08 (Rajasthan — partial), 11 (Sikkim), 12 (Arunachal Pradesh), 13 (Nagaland), 14 (Manipur), 15 (Mizoram), 16 (Tripura), and 17 (Meghalaya) are classified as Special Category States under Article 279A of the Constitution. These states have a lower GST registration threshold (₹10 lakh for services, ₹20 lakh for goods) and received additional revenue compensation during GST's transition period. If you supply to or receive from businesses in these states, be aware that their registration threshold is lower — meaning smaller businesses there may already be registered when you might not expect them to be.

GST Audit — What It Is, Who It Affects, and How to Be Ready

The word 'audit' creates anxiety in most business owners. Under GST, an audit is not just a possibility for large corporations — it is a structured compliance mechanism that applies to businesses across different turnover brackets, in different forms. Understanding what kind of GST audit you may be subject to — and what it will look for — is the first step to being genuinely prepared.

What GST Auditors Actually Look For

Whether it's a departmental audit or a self-initiated annual return, the areas under scrutiny are consistent. Here's where most GST discrepancies are found:

ITC Eligibility and Claim Accuracy

- Is every ITC claim supported by a valid tax invoice from a GST-registered supplier?

- Are ITC claims reconciled with GSTR-2B? Any excess claimed over GSTR-2B is immediately flagged.

- Has ITC been claimed on blocked credit items (Section 17(5))?

- Has ITC been reversed where supplier payment was pending beyond 180 days?

- Has ITC been reversed proportionally for supplies used for both taxable and exempt purposes?

Output Tax Accuracy

- Are all taxable supplies captured in GSTR-1? Are there sales missing from returns (detected by comparing bank deposits with return data)?

- Are the correct GST rates applied to each category of supply? Wrong rate invoicing — even unintentional — leads to short-payment of tax.

- Is the time of supply correctly determined? GST must be charged at the right point — on invoice date, payment date, or delivery date, whichever is earliest for goods.

E-Invoicing Compliance

- For eligible taxpayers, do all B2B invoices have valid IRNs?

- Are there any backdated invoices that bypass the IRP system?

- Is the QR code on physical/PDF invoices matching the IRN in the system?

Reconciliation Between Books and Returns

- Does the turnover declared in GST returns match the turnover in financial statements?

- Does the ITC claimed in GSTR-3B match what's in the purchase register and GSTR-2B?

- Are credit notes and debit notes properly reflected in both GSTR-1 and the books?

GST Reconciliation — The Monthly Discipline That Protects Your ITC

GST reconciliation is the process of matching data across your books of accounts, your GST returns, and the government-generated statements (primarily GSTR-2B) to ensure they are consistent. It sounds administrative — but for most businesses, it is one of the highest-value financial activities performed every month.

A business that does not reconcile GST data regularly is essentially flying blind. It may be claiming ITC it is not entitled to (creating a future liability with interest), or missing ITC it is entitled to (overpaying tax every month). Neither outcome is acceptable.

The Four Key GST Reconciliations Every Business Must Perform

- Purchase Register vs GSTR-2B (ITC Reconciliation)

This is the most critical reconciliation for cash flow and compliance. GSTR-2B is auto-generated by the government on the 14th of each month and shows all the ITC available to you based on invoices uploaded by your suppliers. Your purchase register shows all the invoices you've recorded in your books.

The reconciliation identifies three types of differences:

|

Scenario |

What It Means |

What to Do |

|

Invoice in your books but NOT in GSTR-2B |

Your supplier has not filed their GSTR-1, or filed it with errors. The ITC is not yet available. |

Contact the supplier to file/correct. Do not claim ITC until it appears in GSTR-2B. Track and follow up monthly. |

|

Invoice in GSTR-2B but NOT in your books |

Supplier has uploaded an invoice you haven't recorded — possibly received late, or belongs to a different period. |

Investigate: verify if the goods/services were received. If valid, record the invoice and claim the ITC. |

|

Invoice in both, but with a value mismatch |

Supplier filed a different amount than what's on your invoice — common with rounding differences or amendments. |

If the difference is small, document it. If material, ask the supplier to amend their GSTR-1. Claim only the amount in GSTR-2B. |

- Sales Register vs GSTR-1 (Output Tax Reconciliation)

Every invoice raised in your books should appear in your GSTR-1 — with the correct GSTIN, HSN code, taxable value, and GST amount.

Run this reconciliation before the GSTR-1 filing deadline each month, not after. Amendments to GSTR-1 are allowed but attract scrutiny — it's better to catch errors before filing than to amend repeatedly.

- GSTR-3B vs GSTR-1 (Self-Reconciliation)

GSTR-3B is your self-assessed summary return — the one that determines your actual tax payment. GSTR-1 is the invoice-level detail return.

The GST department's systems automatically compare GSTR-1 and GSTR-3B for each taxpayer. Persistent large differences generate system-generated scrutiny notices (DRC-01A) without any human intervention. Reconciling these two returns before filing eliminates the risk entirely.

- Annual Return vs Financial Statements (GSTR-9 Reconciliation)

The annual reconciliation — required for GSTR-9 and GSTR-9C — is the most comprehensive.

This annual reconciliation often uncovers errors that accumulated over twelve months of monthly filing. Correcting them requires either payment of additional tax with interest, or carrying forward as reconciling items — each with its own documentation requirement.

GST Reconciliation: Month-by-Month Workflow

|

Timing |

Action |

Output |

|

1st–13th of month |

Download GSTR-2B (available from 14th of previous month). Match against purchase register. |

List of unmatched invoices. Supplier follow-up list. |

|

Before 11th |

Reconcile sales register against GSTR-1 data. Upload any missing invoices. File GSTR-1. |

Clean GSTR-1 with no missing or mismatched invoices. |

|

Before 20th |

Finalise ITC to claim based on GSTR-2B. Check RCM liabilities. Reconcile GSTR-3B vs GSTR-1. File GSTR-3B and pay tax. |

Filed GSTR-3B. Tax payment challan. |

|

End of quarter |

Review blocked credit items. Reverse ITC on unpaid invoices beyond 180 days. Check composition limits if applicable. |

ITC reversal register updated. Quarterly compliance sign-off. |

|

November–December |

Annual reconciliation of GSTR-9. Match full-year GST returns against audited financials. Identify and address differences. |

Filed GSTR-9 (and GSTR-9C if applicable). Annual compliance documentation. |

Final Word: GST Has Changed India's Business Landscape

Eight years since its launch, GST is no longer a new or disruptive force. It is the bedrock of India's commercial tax infrastructure. The businesses that have adapted — that have integrated GST compliance into their accounting systems, that verify GSTINs before transacting, that reconcile ITC monthly, and that file returns accurately and on time — have gained a genuine compliance edge.

The ones that treat GST as an annual headache rather than a monthly operating practice are the ones receiving notices, losing ITC, and paying penalties that far exceed what proper systems would have cost.

GST compliance, done right, is not a burden — it's a discipline that protects your Input Tax Credit, keeps your books audit-ready, and ensures your business can grow without regulatory baggage.