If your business transfers stock between two branches in different states, or provides services to an associate company below market value, GST still applies and the value is determined based on the open market value of those goods or services as per Rule 28 of the CGST Rules. This is governed by Schedule I of the CGST Act, 2017, which lists specific activities deemed as supply without consideration.

In this blog, we will discuss about supply of goods or services between related and distinct persons without consideration.

Related person

The definition of “Related Person” is similar to the current Customs Valuation Rules. The supply is considered as between related persons only if the supply of goods or services is made between:

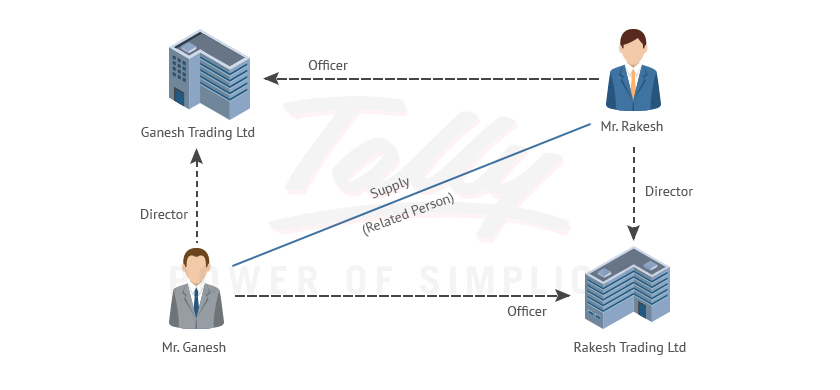

- Officers or directors of one another's businesses: In a supply, the supplier and the recipient are actually officers or directors of the other business.

As illustrated above, Mr. Ganesh is a Director in Ganesh Trading Ltd, and an officer in Rakesh Trading Ltd. Mr. Rakesh, is a Director in Rakesh Trading Ltd. Also, Rakesh is an officer in Ganesh Trading Ltd. Therefore, any supply between them, will be treated as supply between related persons.

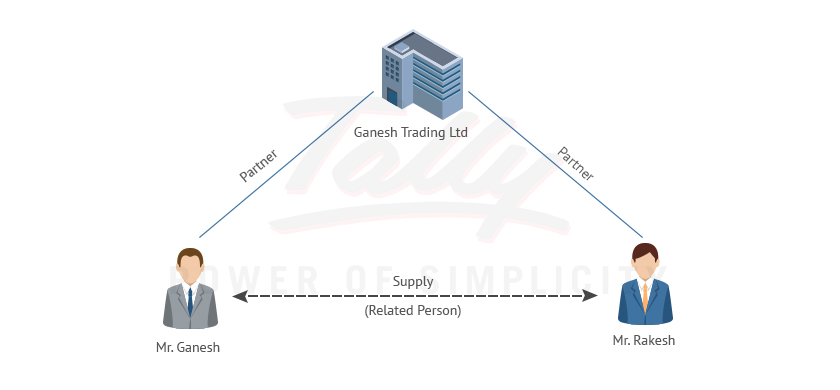

- Legally recognized partners in business: The supplier and the recipient are partners in the same business or associated business.

As illustrated above, Mr. Ganesh and Mr. Rakesh are partners in Ganesh Trading Ltd. Any supply between Mr. Ganesh and Mr. Rakesh will be treated as supply between related persons.

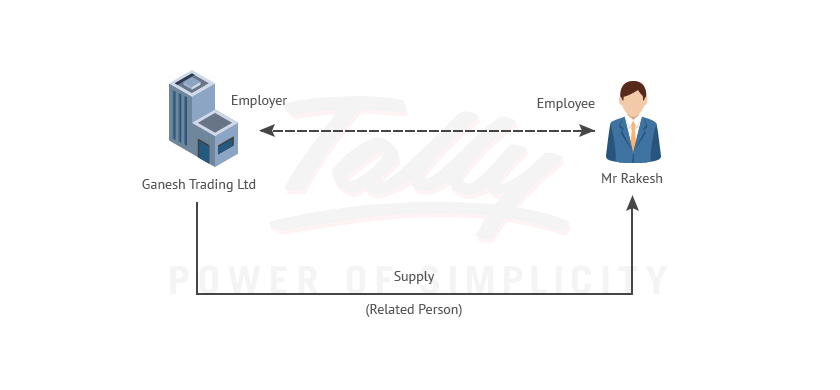

- Employer and employee: Any supply of goods and services between employer and employee.

Mr. Rakesh is an employee of Ganesh Trading Ltd. Any supply from Ganesh Trading Ltd to Mr. Rakesh is considered as supply between related persons.

- The supplier or recipient directly or indirectly owns, controls or holds twenty-five per cent or more of the outstanding voting stock or shares.

For example, the recipient hold 25% of equity in the supplier’s business.

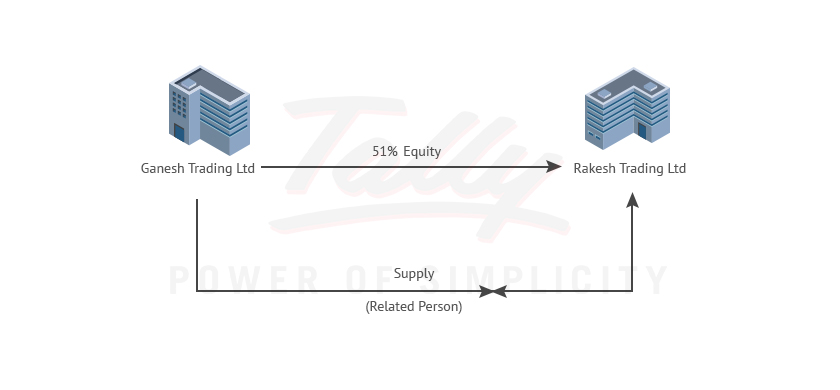

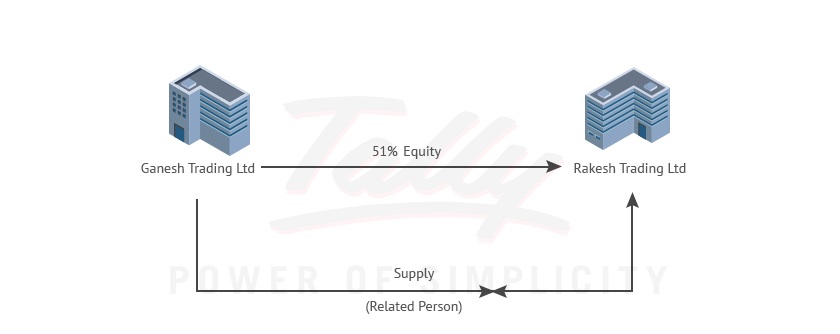

- One of them directly or indirectly controls the other: If in any supply, the supplier or the recipient directly or indirectly controls the other, then it is considered as supply between related persons.

Direct Control

As illustrated above, Ganesh Trading Ltd holds equity in Rakesh Trading Ltd. The supply between Ganesh Trading and Rakesh Trading are related since Ganesh Trading Ltd directly controls Rakesh Trading Ltd.’s business.

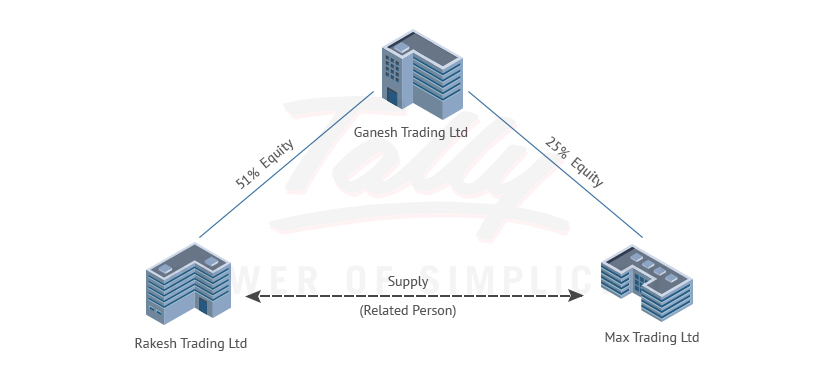

Indirect Control

As illustrated above, Ganesh Trading Ltd holds equity in Rakesh Trading Ltd . Rakesh Trading Ltd. holds equity in Max Trading Ltd. Any supply between Ganesh Trading Ltd and Max Trading Ltd. are related. This is because Ganesh Trading Ltd. indirectly controls Max Trading’s Ltd business by way of ‘Rakesh Trading’s’ business interest in Max Trading Ltd.

- Both of them are directly or indirectly controlled by a third person: If in any supply, the supplier and the recipient are directly or indirectly controlled by a third person.

In the illustration above, Ganesh Trading Ltd holds equity in Rakesh Trading ltd and Max Trading. The supply between Rakesh Trading Ltd and Max Trading ltd are related since both of them are directly controlled by Ganesh Trading Ltd.

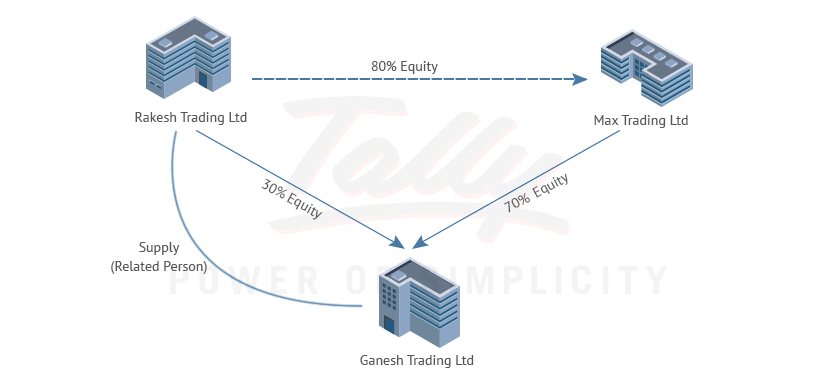

- Together they directly or indirectly control a third person: If in any supply, the supplier and the recipient, together, directly or indirectly control a third person.

As illustrated above, Rakesh Trading Ltd holds 80% equity in Max Trading Ltd and 30% in Ganesh Trading Ltd.

Max Trading Ltd’ hold 70 %equity in Ganesh Trading Ltd . Now, together, Rakesh Trading Ltd has control over Ganesh Trading Ltd and the supply between them will be considered as supply between related persons.

- They are members of the same family: A supply made between the members of the same family is considered as supply between related persons.

Distinct Person

A Distinct Person can be defined as a taxable person who has obtained or is required to obtain more than one registration in the same state or a different state. Or an establishment of a person who has obtained or is required to obtain a registration, and also has the establishment in another state.

Each of his/her registration and establishment will be treated as a Distinct Person, and any supply between them will be taxable.

Therefore, any stock transfer or branch transfers are taxable in the following two cases:

- Intrastate stock transfer: Only when an entity has more than one registration in one state.

Example: Super Cars Ltd is a car manufacturing unit located in Karnataka. They also own a service unit in Karnataka. Super Cars Ltd have obtained separate registrations for both the manufacturing and service units.

The manufacturing unit and the service unit of Super Cars Ltd will be treated as distinct persons, and any supply between them will be taxable, even without consideration.

- Inter-State Stock transfer: Transfer between two entities located in different states is taxable.

Example: Super Cars Ltd is a car manufacturing unit located in Karnataka. They also own a service unit in Delhi.

The manufacturing unit and the service unit of Super Cars Ltd located in Delhi will be treated as distinct persons, and any supply between them will be taxable, even without consideration.

When Does GST Apply? The Schedule I Rule

Schedule I of the CGST Act lists certain activities that are treated as supply even when made without consideration.

Relevant entries under Schedule I:

Entry 1: Permanent Transfer of Business Assets

Permanent transfer or disposal of business assets where ITC has been availed on those assets is a taxable supply — even if done internally.

Entry 2: Supply Between Related or Distinct Persons

"Supply of goods or services or both between related persons or between distinct persons as specified in Section 25, when made in the course or furtherance of business."

This is the big one. Any supply between related or distinct persons even without a rupee changing hands is taxable under GST.

What this means in practice:

| Transaction | Is GST Applicable? |

|---|---|

| Head office provides marketing services to its branch | Yes |

| Parent company transfers goods to subsidiary at cost | Yes |

| Delhi branch sends inventory to Mumbai branch | Yes |

| Company provides free goods to director's family business | Yes |

| Employee receives gifts worth more than ₹50,000 in a year | Yes |

| Employee receives gifts worth ₹50,000 or less in a year | No (exempted) |

The Important Exception: Employee Transactions

Not all employee-related transactions are taxable. The GST law specifically exempts gifts or perquisites given to employees up to ₹50,000 per year per employee.

However, if your company provides services like rent-free accommodation, a company car for personal use, or club memberships to directors — these may qualify as taxable supplies depending on the nature and value.

How Is the Value of Supply Determined?

When a transaction is between related or distinct persons, the price charged may not reflect the actual market value. To prevent undervaluation and tax evasion, GST law prescribes specific valuation rules under Rule 28 of the CGST Rules, 2017.

Rule 28: Valuation for Related and Distinct Person Transactions

The value of supply shall be, in order of preference:

1. Open Market Value (OMV) The price at which such goods or services would be sold to an unrelated buyer in the open market at the same time and in similar conditions.

2. Value of Supply of Like Kind and Quality If OMV is not available, use the value of similar goods or services supplied to unrelated parties.

3. Value Under Rule 30 or Rule 31 Cost-based valuation (110% of cost of production/manufacture) or residual method (best judgement approach).

Special Case: If the recipient is eligible for full ITC, the value declared on the invoice — even if it's ₹1 — is acceptable. This is a significant relief for branch-to-branch transfers where full ITC is available downstream.

Practical Valuation Example

Scenario: ABC Pvt. Ltd. (Mumbai) transfers 500 units of a product to its branch in Delhi. The product sells to customers at ₹1,000 per unit. The company wants to invoice the transfer at ₹600 per unit.

| Valuation Basis | Taxable Value | GST @18% |

|---|---|---|

| Invoice value (₹600/unit) | ₹3,00,000 | ₹54,000 |

| Open market value (₹1,000/unit) | ₹5,00,000 | ₹90,000 |

If the Delhi branch is eligible for full ITC, ₹3,00,000 (invoice value) is acceptable. If not, the open market value of ₹5,00,000 must be used.

ITC (Input Tax Credit) Implications

One of the most important downstream effects of related/distinct person transactions is on input tax credit.

When ITC Can Be Claimed

- The recipient (branch or subsidiary) can claim ITC on the tax invoice raised by the supplier

- Full ITC is available if the goods/services are used for business purposes

- If the Delhi branch sells the received goods to end customers, it can claim the IGST paid on the stock transfer

When ITC Gets Blocked or Reversed

- If goods are used for exempt supplies at the receiving end, proportionate ITC must be reversed

- ITC is blocked on goods/services used for personal consumption (Section 17(5))

- If the invoice is not raised or incorrectly raised, ITC claim by recipient can be denied

CA Advisory: Always ensure that tax invoices for inter-branch or related-party transactions are raised within the time limits prescribed under GST law. A missing or late invoice can cascade into ITC denial for the recipient entity.

GST Documentation Checklist for Related/Distinct Person Transactions

Here's what every business must maintain:

- Tax Invoice — with correct GSTIN of both supplier and recipient

- Valuation Working — documented basis for the price charged (OMV, cost+, etc.)

- E-way Bill — for movement of goods above ₹50,000

- ITC Reconciliation — matching GSTR-2B with purchase register

- Transfer Pricing Documentation — for transactions with international related parties

- Board Resolution / Agreement — for service arrangements between group companies

- GSTR-1 Reporting — all such supplies must be reported correctly

Common Mistakes Businesses Must Avoid

| Mistake | Risk |

|---|---|

| Not raising an invoice for branch-to-branch transfers | ITC denial + penalty |

| Undervaluing supply to related party without ITC eligibility check | Demand notice + interest |

| Treating group company transactions as exempt | GST demand + 18% interest |

| Missing e-way bill for stock transfers | ₹10,000 fine or tax evaded (whichever is higher) |

| Reporting related-party supplies incorrectly in GSTR-1 | Mismatch notices |

| Not reconciling ITC on related-party purchases | Audit risk |