As a business owner, understanding depreciation is crucial for accurate expense tracking and maximising tax benefits. Depreciation allows you to spread the cost of an asset over its useful life, reducing taxable income in the early years. Failing to account for depreciation properly can lead to poor financial decisions.

This guide covers the fundamentals of depreciation, different calculation methods, and real-world examples across industries. Mastering depreciation is essential for informed decision-making and steering your business towards success and efficiency.

What is depreciation?

Depreciation is the accounting process of spreading the cost of a fixed asset over its useful life. It reflects how an asset loses value over time through use, wear and tear, or obsolescence. Instead of expensing the full cost upfront, a portion is expensed each year.

Say a restaurant buys a new commercial oven for ₹1,00,000 with a projected lifespan of ten years. Under straight-line depreciation, it records an expense of ₹10,000 each year for ten years, instead of deducting the full ₹1,00,000 in year one. The cost is spread across the asset's working life.

Why is depreciation important for businesses?

Common depreciable assets include machinery, vehicles, buildings, computers, office equipment, and furniture. These assets generate income but steadily lose value and usefulness. Depreciation lets businesses recover the cost of these investments as they earn revenue.

Depreciation directly affects cash flow and tax liability. Higher depreciation means lower taxable income, which reduces the tax you pay now. Each year, the depreciation expense reduces net income on the income statement.

This improves cash flow in the early years of an asset's life. For businesses making large capital purchases, maximising depreciation where applicable is an important tax strategy.

How to calculate depreciation

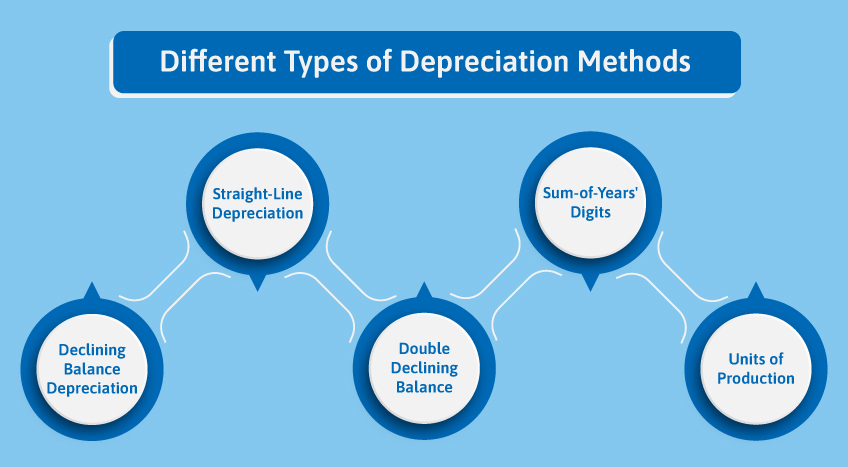

Different types of depreciation methods

Understanding the fundamentals of accounting includes knowing the main methods of calculating depreciation expenses.

The most prevalent forms of depreciation include:

Straight-line depreciation

Under the straight-line method, the same depreciation expense is recorded each year over the asset's useful life, until it reaches its salvage value. It is the most common and simplest approach.

For example, take equipment costing ₹50,000 with a 10-year life and a ₹5,000 salvage value. The depreciable amount is ₹45,000 (₹50,000 − ₹5,000), so depreciation is ₹4,500 per year. That works out to 10% of the depreciable amount every year.

Declining balance depreciation

This accelerated method charges more depreciation in the early years of an asset's life. Each year, the expense is a fixed percentage of the asset's book value.

Take a 25% declining balance rate on a ₹50,000 asset. Year one depreciation is 25% of ₹50,000 = ₹12,500. Year two is 25% of the remaining ₹37,500 book value = ₹9,375.

Double declining balance (DDB)

DDB doubles the declining balance rate, accelerating depreciation even further. In the example above, annual depreciation would be 50% of book value instead of 25%. This front-loads even more of the expense into the asset's early years.

Sum-of-years' digits (SYD)

Like declining balance methods, SYD charges more depreciation in the early years. The annual rate is a fraction based on the sum of the digits of the asset's useful life.

Units of production

This method links depreciation to actual usage, basing the annual expense on real output. The depreciable cost is divided by the expected lifetime units to get a per-unit depreciation cost.

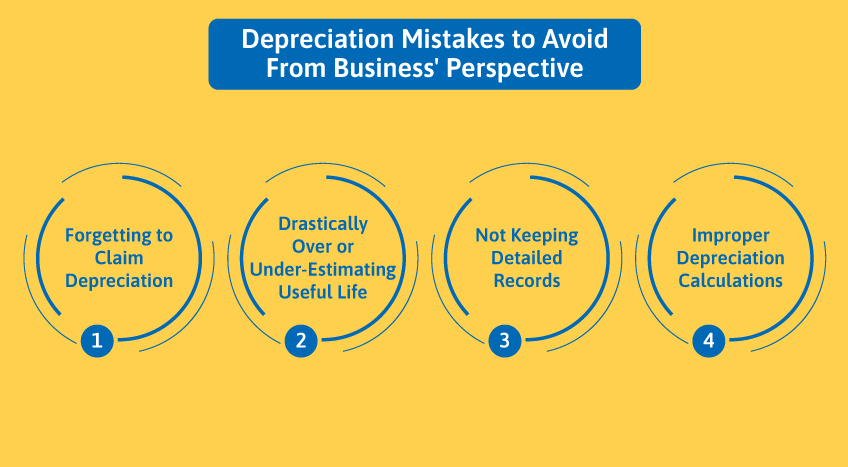

Depreciation mistakes to avoid from a business's perspective

Avoiding repeated depreciation mistakes helps you get a better understanding and hold of the financial position of your business.

The first step in avoiding depreciation mistakes is a strong grasp of accounting fundamentals.

The common mistakes to watch for are:

Forgetting to claim depreciation

Neglecting depreciation overstates profits and asset book values. Properly tracking fixed assets and maximising depreciation deductions is essential for accurate financials.

Drastically over- or under-estimating useful life

Your useful-life estimate directly drives the depreciation charge. Overestimating it spreads the cost too thin and delays deductions, while underestimating it charges too much depreciation too early. Use asset categories, industry standards, and regular reviews to set realistic, compliant useful lives.

Not keeping detailed records

Keep detailed records for every fixed asset: purchase date, cost, depreciation method, useful life, and accumulated depreciation. Good records make each year's calculation accurate. Without proper documentation, errors and missed deductions become far more likely.

Improper depreciation calculations

With multiple methods available, such as straight-line, declining balance, and units of production, calculations can get complicated. Formula errors lead to inaccurate depreciation expenses.

Double-check every calculation and the method applied. Consulting an accounting professional helps reduce errors and claim valid deductions fully.

Examples of depreciation in business

1. Machinery

A factory machine loses value over time due to wear and tear.

Depreciation is charged yearly as a business expense.

2. Vehicles

Company cars or delivery vans depreciate due to usage and age.

3. Office Equipment

Computers, printers, and furniture lose value over time due to usage and technological changes.

4. Buildings

Commercial buildings depreciate over long periods (excluding land).

Wrapping up

Every business owner needs to understand depreciation. Spreading asset costs over their useful lives accounts for use and obsolescence. Getting it right improves cash flow, reduces taxes, and strengthens financial reporting.

Avoid the common pitfalls: not claiming depreciation, misjudging useful lives, poor asset records, and calculation errors. TallyPrime automates depreciation calculations, maintains asset records, and generates financial reports in line with Indian accounting rules.

By understanding depreciation and using software like TallyPrime, business owners can make smarter decisions and get the full tax advantage from their fixed assets.