Accounting helps a business track income and expenses, stay statutorily compliant, and give investors reliable financial information. It keeps the books balanced and supports growth. To do this well, every entrepreneur must understand two methods: cash accounting and accrual accounting.

The choice between cash and accrual accounting is crucial. The distinction may seem simple, but it affects funding, tax compliance, profitability analysis, and planning.

This guide explains the primary differences between the two methods and why each matters.

Importance of cash accounting for business and entrepreneurial success

Cash accounting is a bookkeeping method where transactions are recorded only when cash changes hands. Revenue is recorded when cash is received from customers, and expenses when bills are paid. This makes it very simple for small businesses to understand and use.

Since transactions are recorded as cash comes in or goes out, owners always know their current cash position. Many sole proprietors and small businesses prefer cash accounting for this simplicity. There are no unpaid invoices to record and no payables or receivables to track.

Cash accounting: key advantages for business owners

The prime advantage of cash accounting is its simplicity. Preparing accounts is easier because firms need fewer year-end adjustments.

But these are not the only benefits:

Ease of cash flow tracking

Cash accounting gives business owners a simple way to track cash inflows and outflows in real time. Because transactions are recorded only when cash changes hands, you always know the company's liquidity position. It also makes it easy to see how much cash is available for daily expenses.

Alignment with cash-based operations

In their early years, many sole proprietorships and partnerships run mostly on cash. Cash accounting suits them well, since revenue is recognised only when customers pay. Because revenue and expenses line up with actual cash movement, financial reporting stays simple.

Low compliance burden

In the early stages, when transactions are few, cash accounting creates very little accounting work. Entrepreneurs get more time to focus on growing the business. Financial statements need only minor adjustments, which keeps compliance simple and low-cost for small businesses.

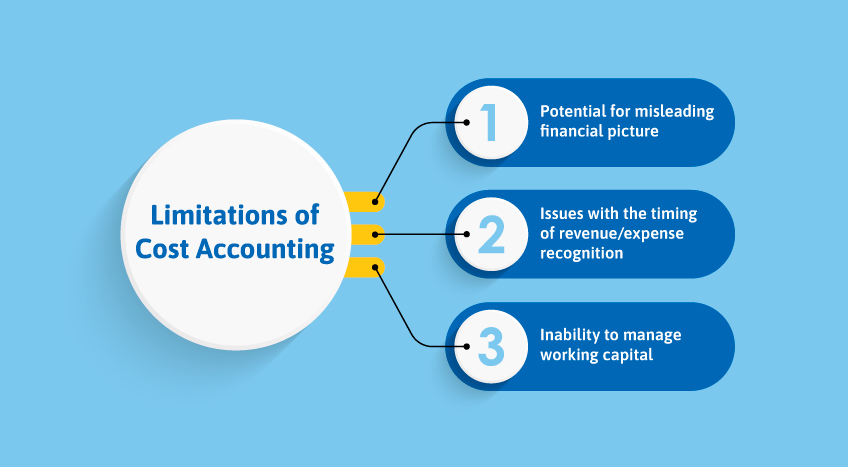

Limitations of cash accounting business owners must consider

For as many benefits as cash accounting offers, there are a few limitations that business people and entrepreneurs have to deal with. The primary limitations of cash accounting include:

- Potential for misleading financial picture: Cash accounting shows your current cash position clearly, but not the complete financial picture. Because receivables and payables are excluded, it cannot accurately indicate long-term financial health, such as profitability.

- Issues with the timing of revenue/expense recognition: Revenue is recognised only when cash is received, not at the point of sale or service. This timing gap can distort the financial results reported to owners and tax authorities.

- Inability to manage working capital: Cash accounting does not record amounts owed to suppliers or owed by debtors. Without payables and receivables, you cannot see the working capital tied up in the business.

Accrual accounting for business owners: what you need to know

Accrual accounting records transactions when the economic activity happens, regardless of when cash moves. This gives business owners an accurate picture of the financial situation.

Expenses are recorded when goods or services are consumed, or a liability arises. Revenue is recorded in the period the sale is made or the service is delivered, even if full payment has not yet been received.

By recording unpaid expenses as accruals and money owed to the business as receivables, accrual accounting shows a fuller financial position at any moment. It matches revenues with the costs incurred to earn them, revealing true profitability. This helps owners and executives make better-informed decisions.

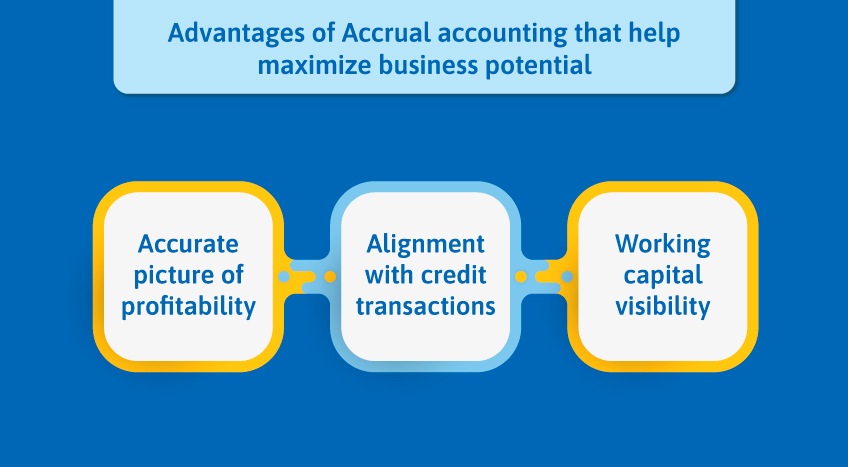

Advantages of accrual accounting that help maximise business potential

Accrual accounting offers a set of advantages that differ from cash accounting. The most prominent advantages of accrual accounting are:

- Accurate picture of profitability: Recording revenues when earned and expenses when incurred gives an accurate view of long-term profitability. This supports better decisions on investments, pricing, and operations.

- Alignment with credit transactions: Many established businesses sell on credit. Accrual accounting fits this model, recognising revenue on credit sales when the transaction is completed rather than when payment arrives.

- Working capital visibility: Tracking payables and receivables shows the working capital invested in the business. This helps you manage inventory, debtors, credit terms, and cash flow as you scale.

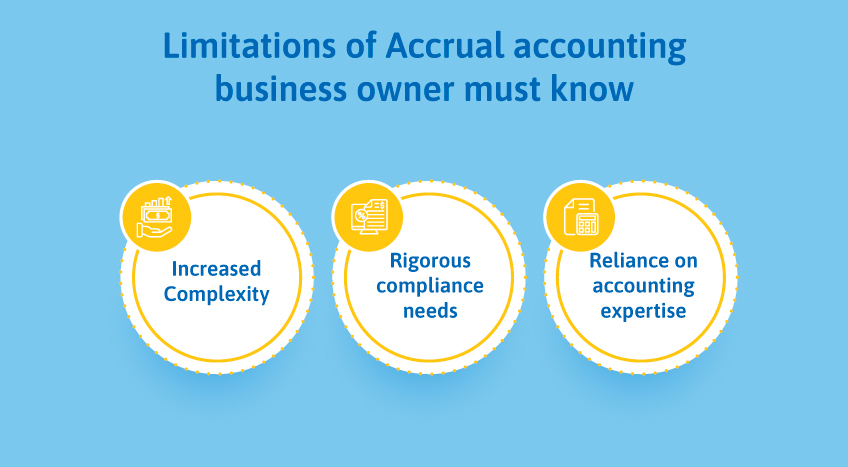

Limitations of accrual accounting that business owners must know

Like cash accounting, accrual accounting also carries its own set of limitations. Some of the most eminent limitations of accrual accounting are:

- Increased Complexity: Accrual accounting offers a fuller financial view than cash accounting, but it is more complex. Computing accruals and deferrals takes skill and diligence.

- Rigorous compliance needs: You must follow accrual accounting principles and tax rules carefully to avoid penalties. This means maintaining accurate daily records of invoices, receipts, expenses, and other transactions.

- Reliance on accounting expertise: Accrual accounting demands more expertise than cash accounting, especially in tracking receivables, payables, and inventory. Growing businesses often need to hire or outsource accounting professionals to stay compliant.

Difference between cash accounting and accrual accounting: comparative analysis for business owners

The prime difference is timing. Cash accounting records revenue when cash is received and expenses when cash is paid. Accrual accounting records income when it is earned and costs when they are incurred.

Here are the key differences:

|

Criteria |

Cash Accounting |

Accrual Accounting |

|

Timing of Revenue Recognition |

Recognised when cash is received from customers |

Recognised when the sale is made, or service is delivered, even if full payment is not received |

|

Timing of Expense Recognition |

Recognised when bills are paid in cash |

Recognised when costs are incurred, regardless of when payment is made |

|

Treatment of Receivables |

Not recorded as accounts receivable |

Amounts owed by debtors are recorded as accounts receivable |

|

Treatment of Payables |

Not recorded as accounts payable |

Amounts owed to creditors are recorded as accounts payable |

|

Financial Statements |

Can provide a misleading view of long-term profitability |

Provides an accurate picture of profitability by matching revenues to expenses |

|

Suitable for |

Small sole proprietorships and businesses with cash transactions |

Growing businesses, especially those with credit sales and complex operations |

Final takeaways

Cash accounting is easier because it tracks only cash transactions. Accrual accounting gives a more realistic picture of long-term performance by matching revenues with expenses. The right choice depends on your business's size, operations, and financial goals. For sole proprietorships and small businesses, cash accounting keeps compliance simple.

Whichever method you choose, efficient accounting software is essential. TallyPrime is integrated, GST-compliant software that handles both cash and accrual accounting. It helps you manage accounts, meet tax and accounting standards, and get insightful reports for financial oversight.