- Budgeting and Budget

- What is Capital Budgeting?

- Capital Budgeting Examples and Calculations

- Capital Budgeting Process

Budgeting and Budget

Budgeting is a management tool for planning and controlling future activity. It is a plan for saving, borrowing and spending which the management works out to finance its projects or to check the financial viability of its projects by evaluating its costs and benefits.

While the budgeting is a larger tool, a budget is a financial plan with lists of all planned expenses and revenue.

What is Capital Budgeting?

Capital budgeting is a process through which different projects are evaluated in terms of cost and benefits. It is the firm’s formal process for acquisition and investment of capital. It involves decisions to invest its current funds for addition, disposition, modification and replacement of fixed assets.

Capital Budgeting Examples and Calculations

Example -1

Max limited is looking to invest in a new project and the cost of the project is Rs. 12,000 /-. Before investing, they want to analyze that how long it will take to recover invested money in a project?

Estimated profit for first and the subsequent year is given below:

|

Year |

Profits ( Amount in Rs. ) |

|

First Year |

Rs. 3,000 |

|

Second Year |

Rs. 3,000 |

|

Third Year |

Rs. 3,000 |

|

Fourth Year |

Rs. 3,000 |

Looking at the above table, one can make out that a company can recover the invested money in 4 years. But this is not the right way to find out a payback period of the initial investment. Here, the company is considering profit and not the net cash flows. In order to arrive at the payback period, you should use net cash flow.

As we know that profit is arrived after deducting depreciation and other non-cash expenses, so to know the correct net cash flows, we must add depreciation and other non-cash expenses to profits.

Let’s say depreciation value is Rs. 2,000 /-

The net cash flow after considering deprecation is given below:

|

Year |

Profits (Amount in Rs. ) |

Depreciation |

Cash flows before Depreciation |

Cumulative Cash flows |

|

First Year |

Rs. 3,000 |

Rs. 2,000 |

Rs. 5,000 |

Rs. 5,000 |

|

Second Year |

Rs. 3,000 |

Rs. 2,000 |

Rs. 5,000 |

Rs. 10,000 |

|

Third Year |

Rs. 3,000 |

Rs. 2,000 |

Rs. 5,000 |

Rs. 15,000 |

|

Fourth Year |

Rs. 3,000 |

Rs. 2,000 |

Rs. 5,000 |

Rs. 20,000 |

From the above analysis, a company will recover the initial investment in 2 years and few months. To arrive exact payback period, the following formula can be used:

Payback period = Investment Required/ Net Annual Cash Flow

12,000/5,000 =2.4 years

Here, the payback period is nothing, but the time taken to recover the investment amount. The above payback period can be applied if the annual net cash flow is even. In case of uneven net cash flow, the calculation applied in below example can be used.

Example -2

The cost of the project is 12,000 and below is the next cash flow per annum.

|

Year |

Net Cashflow |

|

First Year |

Rs. 5,000 |

|

Second Year |

Rs. 3,000 |

|

Third Year |

Rs. 7,000 |

|

Fourth Year |

Rs. 3,000 |

|

Year |

Profits (Amount in Rs. ) |

Investment yet to be recovered |

|

First Year |

Rs. 5,000 |

Rs. -7,000 (5,000 – 12,000) |

|

Second Year |

Rs. 3,000 |

Rs. -4,000 (3,000-7,000) |

|

Third Year |

Rs. 7,000 |

Rs. +3,000 (7,000-4,000) |

|

Fourth Year |

Rs. 3,000 |

Rs. +6,000 |

If you look at the above example, the initial investment of 12,000 is recovered in 2+ years. To know the exact pay period, use the below calculations:

2 +( 4,000/7,000) = 2.7 years

Here, 2 is the second year which last had a negative value indicating some initial investment yet to be recovered. 4,000 is the amount left for recovery at the end of the second year and 7,000 is net cash flow of the third year. So, you need to divide 4,000 by 7,000 to know the no. of months you would take to earn this 4,000 in the third year.

The other popular methods for evaluating project proposal are Net Present Value method and Internal Rate of Return method.

Take a look at Tips for Efficient Capital Expenditure Practices

Features of Capital Budgeting:

- Capital Budgeting involves potentially large anticipated benefits.

- Its involves a high degree of risk due to high cash outlay and planned for a longer period.

- It also involves a long gestation period between the initial outlay and the anticipated return.

Capital Budgeting Process

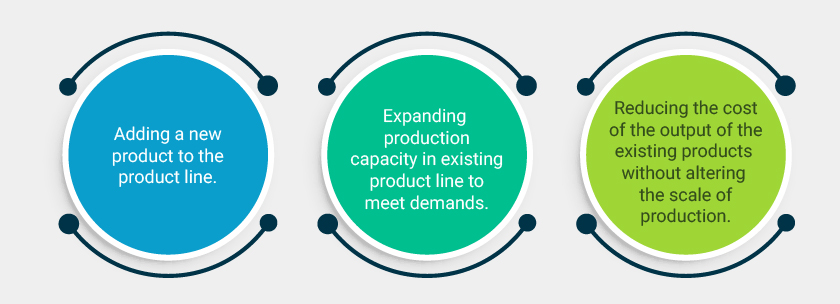

Project Generation

Generating a proposal for investment is the first step in the capital budgeting process. The proposal may fall into one of the following categories.

Project Evaluation

It is the crux of capital budgeting where a project undergoes cost-benefit analysis considering the risks and future uncertainties associated. It generally involves two-step analysis.

Project Selection

There is no standard administrative procedure to guide the management to select the best project among the bests or approving a correct investment proposal. The screening and selection procedures for selecting a project differ from firm to firm.

Acquiring funds for the project

Once a project proposal is finalized by the management or the management agrees with the capital expenditure for the project, the finance manager then explores the different alternatives available for acquiring the funds.

The manager then prepares the capital budget with an approach to reduce the average cost of funds so that the project is available for selection or attracts the interest of the management.

He also prepares a periodical report which helps in reviewing the performance of the projects which will help the management to make informed decisions throughout the project’s lifetime, and even after completion when they go for another project with the same selection criteria.

Follow up proposal

In the follow-up proposal, comparison of actual performance with original estimates is carried out. It not only ensures better forecasting but also helps in sharpening the techniques for improving future forecasts.

Major capital projects involving huge amounts of money, as well as capital expenditures, can get out of control quite easily if mishandled and end up costing an organization a lot of money. However, with effective planning, the right tools, and good project management, that doesn’t have to be the case. Take a look at Tips for Efficient Capital Expenditure Practices