Keeping track of financial activities is important for business owners and entrepreneurs to better balance their accounts. It also helps maintain precision, uniformity, and adherence to accounting standards.

One accounting fundamental that helps business owners achieve this efficiently is the accounting cycle. It is a series of steps to record, classify, summarise, and report business transactions within a given accounting period.

The accounting cycle documents, summarises, and reports financial transactions to provide business owners with meaningful financial information. Although the cycle may appear complicated, it produces realistic financial results that reveal your company's success.

Understanding this cycle helps you use financial data for decision-making and accounting efficiency. Let's break down the phases to simplify the accounting cycle and maximise its commercial benefits.

Accounting cycle for financial management

The accounting cycle is the process of recording, summarising, and reporting a company's financial transactions over a specific period. It systematically documents all business activities, converting raw data into meaningful financial statements.

These statements provide critical insights into the company's performance, enabling informed decision-making.

The accounting cycle is more than number crunching. It is a strategic tool for understanding your business's financial health.

Owners who understand it can use financial data to track progress, reduce risks, spot opportunities, and grow sustainably. It also makes data-driven decisions easier, which is invaluable for long-term success.

Benefits of an efficient accounting cycle

From budgeting to expense tracking, the accounting cycle supports business owners across their financial goals. It also improves accuracy and efficiency.

The primary benefits of an efficient accounting cycle for business owners are:

- Accurate financial reporting: Generates error-free, audit-ready financial statements through rigorous adherence to accounting principles.

- Up-to-date visibility into business performance: Enables real-time monitoring of crucial metrics and trends by processing transactions as they occur.

- Data-driven strategic decision-making: Provides validated financial data and analytics to inform pricing, budgeting, growth strategies, and more.

- Measuring past financial strategies' effectiveness: Allows comprehensive evaluation of previous tactics based on historical performance data.

- Compliance with accounting standards and regulations: Ensures adherence to accounting standards and legal obligations.

- Accurately reflecting business performance: Results in precise financial statements that thoroughly depict the company's operations.

Steps in the accounting cycle process

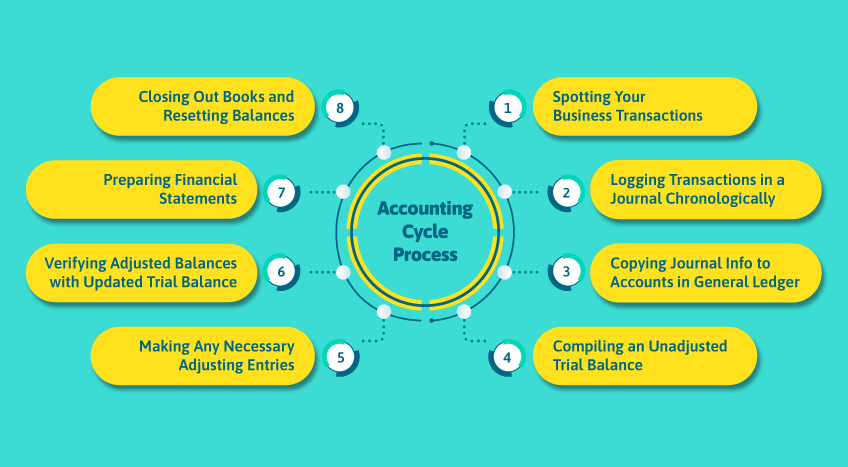

The eight-step accounting cycle is critical for every accountant and business owner to understand. These divided tasks include the following steps:

Step 1: Spotting your business transactions

The accounting cycle starts with identifying every financial transaction your business made during the period. This includes sales, purchases, payroll, income, and expenses. Each of these affects your financial position. Record every transaction, no matter how small. Even a cup of coffee bought for a client meeting counts. Careful recording of every transaction lays the foundation for accurate accounting.

Step 2: Logging transactions in a journal chronologically

Once you identify all transactions, record them in a journal by date. This creates a timeline of your financial activities. Each journal entry uses debits and credits to show which accounts the transaction affects. The journal gives you an organised history you can refer back to whenever needed.

Step 3: Copying journal info to accounts in the general ledger

Next, post the journal entries to the general ledger to update each account's balance. The general ledger holds a complete record of all transactions for the period, broken down by account. Grouping transactions by account makes it easy to see where each account stands.

Step 4: Compiling an unadjusted trial balance

Before preparing financial statements, list the balances of all general ledger accounts in an unadjusted trial balance. This is a first check. It helps you spot and fix ledger errors before moving to the next steps. Think of it as a dress rehearsal before the main performance.

Step 5: Making any necessary adjusting entries

Adjust journal entries where needed so they follow accounting principles and match revenues with expenses. Common adjustments in accrual accounting include depreciation, allowance for doubtful debts, prepaid expenses, and unearned revenue. These adjustments give a more accurate picture of your finances.

Step 6: Verifying adjusted balances with updated trial balance

Once all adjusting entries are in, prepare an adjusted trial balance. This confirms that debits and credits are still equal after the adjustments. You can then fix any remaining errors before preparing the official financial statements.

Step 7: Preparing financial statements

Once the adjusted trial balance is accurate, prepare the official financial statements. These typically include the income statement, balance sheet, cash flow statement, and statement of retained earnings.

Step 8: Closing out books and resetting balances

At the end of the accounting period, close the accounts to complete the cycle. Closing entries reset temporary accounts, such as revenues, expenses, and dividends, back to zero. This resets the books and starts a new accounting cycle.

Wrapping up

Mastering the accounting cycle provides vital visibility into your business's financial health and performance. By systematically recording, processing, and reporting transactions, you gain data-driven insights crucial for driving growth and success.

While manual accounting can be tedious, leveraging solutions like Tally Solution can automate and streamline the cycle through real-time updates and seamless integration. Implementing an efficient accounting cycle, whether manually or through software, is essential for monitoring financial performance and positioning your business for long-term prosperity.