If you pay a year's worth of expenses upfront (maybe you made an annual rent payment in January), it ideally shouldn't all reflect on your income statement that same month. It’s not an accurate reflection of this situation, and that's why we have prepaid expenses accounting.

Instead of booking advance payments for goods or services as expenses immediately, businesses record them as current assets on the balance sheet. As the prepaid benefit is used up, adjusting entries gradually shift the balance from assets to expenses, period by period, until nothing remains to carry forward. If handled any less delicately, your profit figures, balance sheet and financial records all drift out of sync with reality.

This accounting treatment follows the matching principle, which mandates that expenses be recognised in the same period as the revenue they support, ensuring financial statements present a more accurate picture of business performance. Without this measure, a single large upfront payment can make one quarter look worse than it is, and the next few look better than they actually are.

(This image was created using AI)

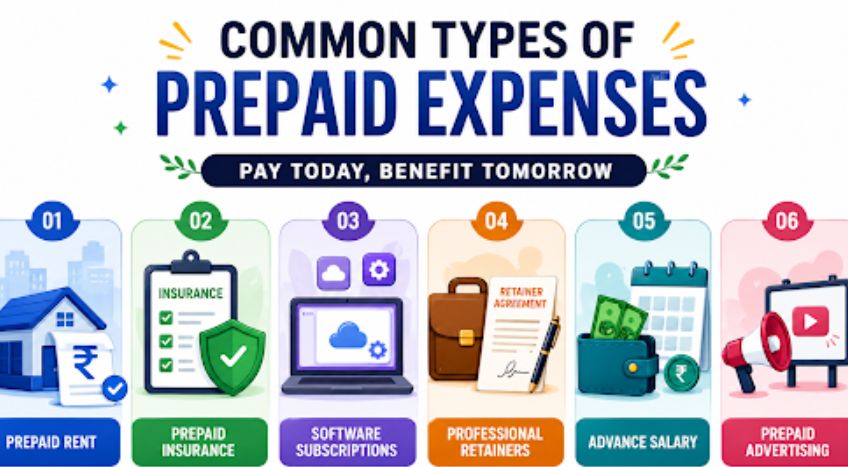

Businesses often incur prepaid expenses by paying in advance for goods or services that provide benefits over multiple accounting periods. Examples include:

- Prepaid rent: Advance payments made to a landlord before the rental period begins.

- Prepaid insurance: Insurance premiums paid upfront for coverage extending beyond the current accounting period.

- Software subscriptions: Annual licences or SaaS tools billed upfront for services used over future periods.

- Professional retainers: Fees paid in advance to lawyers, consultants or chartered accountants for future services.

- Prepaid advertising: Advertising costs paid upfront for campaigns scheduled to run in future periods.

- Training subscriptions: Annual training or e-learning programmes paid upfront but accessed over time.

How are prepaid expenses recorded?

Prepaid expenses are recorded in two stages: first, the advance payment is recognised as an asset because the business will receive the benefit in future periods and later, the amount is gradually recognised as an expense as the benefit is consumed through adjusting entries.

Initial entry

When a prepaid expense is paid, it is recorded as a prepaid asset rather than an expense because the related service or benefit has not yet been used.

For example, suppose a business pays ₹24,000 on 1 April for a 12-month insurance policy.

|

Account |

Debit (₹) |

Credit (₹) |

|

Prepaid Insurance A/c |

24,000 |

|

|

Cash/Bank A/c |

|

24,000 |

At this stage, no expense has been recognised because the insurance coverage will be consumed over future periods. Therefore, the ₹24,000 remains recorded as an asset on the balance sheet.

Adjustment entry

As the prepaid benefit is consumed over time, adjusting entries transfer the applicable portion from the asset account to the expense account. This is done at the end of each accounting period.

For the insurance example above, ₹2,000 worth of insurance is consumed each month (₹24,000 ÷ 12).

|

Account |

Debit (₹) |

Credit (₹) |

|

Insurance Expense A/c |

2,000 |

|

|

Prepaid Insurance A/c |

|

2,000 |

This adjustment reduces the prepaid insurance balance and records the same amount as an expense in the income statement. The process continues each period until the prepaid balance is fully consumed.

After 12 months, the prepaid insurance account reaches zero and the full ₹24,000 is recognised as an insurance expense, ensuring the expense is recorded in the period in which the benefit is received.

How do prepaid expenses affect financial statements?

Prepaid expenses affect both the balance sheet and income statement because they are initially recorded as assets and gradually recognised as expenses over time.

- Balance sheet: Prepaid expenses appear under current assets. As adjusting entries are passed each period, the prepaid balance reduces. Once fully consumed, the asset balance is zeroed out, and the line item disappears.

- Income statement: Only the portion consumed during the current accounting period is recognised as an expense. This prevents large upfront payments from distorting profits in a single period.

Important: The initial payment entry does not affect profits because it is recorded as an asset. Only the adjusting entries impact the income statement by recognising expenses over time.

How are prepaid expenses treated under Indian Accounting Standards?

The accrual basis of accounting is mandatory under the Companies Act, 2013, which requires expenses to be recognised in the period in which the related benefit is received, regardless of when payment is made. This treatment applies whether a business follows AS (Accounting Standards) or Ind AS (Indian Accounting Standards).

- Under AS 1 (Disclosure of Accounting Policies), businesses need to follow the accrual basis of accounting. As a result, payments made in advance cannot be recognised as expenses immediately; they must first be recorded as assets and gradually expensed over the relevant period.

- The same principle applies to companies following Ind AS, where expenses are recognised only when the associated economic benefits are consumed.

From a compliance perspective, prepaid expenses should be reviewed and adjusted regularly to ensure expenses are recognised in the correct accounting period. During statutory audits, material unadjusted prepaid balances or weaknesses in related accounting controls may attract auditor scrutiny and require further explanation. Accurate treatment of prepaid expenses also enhances the reliability of financial statements for lenders, investors and other stakeholders.

How do prepaid expenses affect working capital?

Prepaid expenses affect working capital because they are classified as current assets, even though they do not represent cash or funds that are immediately available. Large or poorly managed prepaid balances can therefore inflate working capital figures without reflecting actual liquidity.

For example, a business showing ₹5,00,000 in current assets may have ₹1,50,000 tied up in prepaid expenses, funds that cannot be used for operations, supplier payments or emergencies.

Keeping prepaid balances lean and ensuring timely adjustments helps prevent working capital from appearing stronger on paper while remaining tight in practice.

It is also important to consider materiality when accounting for prepaid expenses. Small advance payments that are not material to the financial statements may sometimes be expensed immediately in accordance with an entity’s accounting policies, provided such treatment does not materially affect financial reporting.

Conclusion

Accurate accounting for prepaid expenses hinges on passing journal entries correctly. It’s about ensuring that profits, working capital and financial statements echo the true financial position of a business.

As businesses grow and manage multiple prepaid expenses across rent, insurance, software and subscriptions, maintaining this consistency becomes increasingly important. TallyPrime simplifies prepaid expense tracking, automates adjusting entries and helps businesses maintain accurate financial records more efficiently. Manage your accounts with confidence using TallyPrime, trusted by more than 2.7 million businesses across India.