The fixed asset headache

In my 20 years as a Senior Accountant, I’ve found that many small business owners treat fixed assets like a "set and forget" entry. This is a costly mistake. Losing track of asset values means you are literally leaving tax benefits on the table. TallyPrime is the essential tool for tracking these values and automating tax-compliant depreciation entries, provided you set up your workflows correctly from day one.

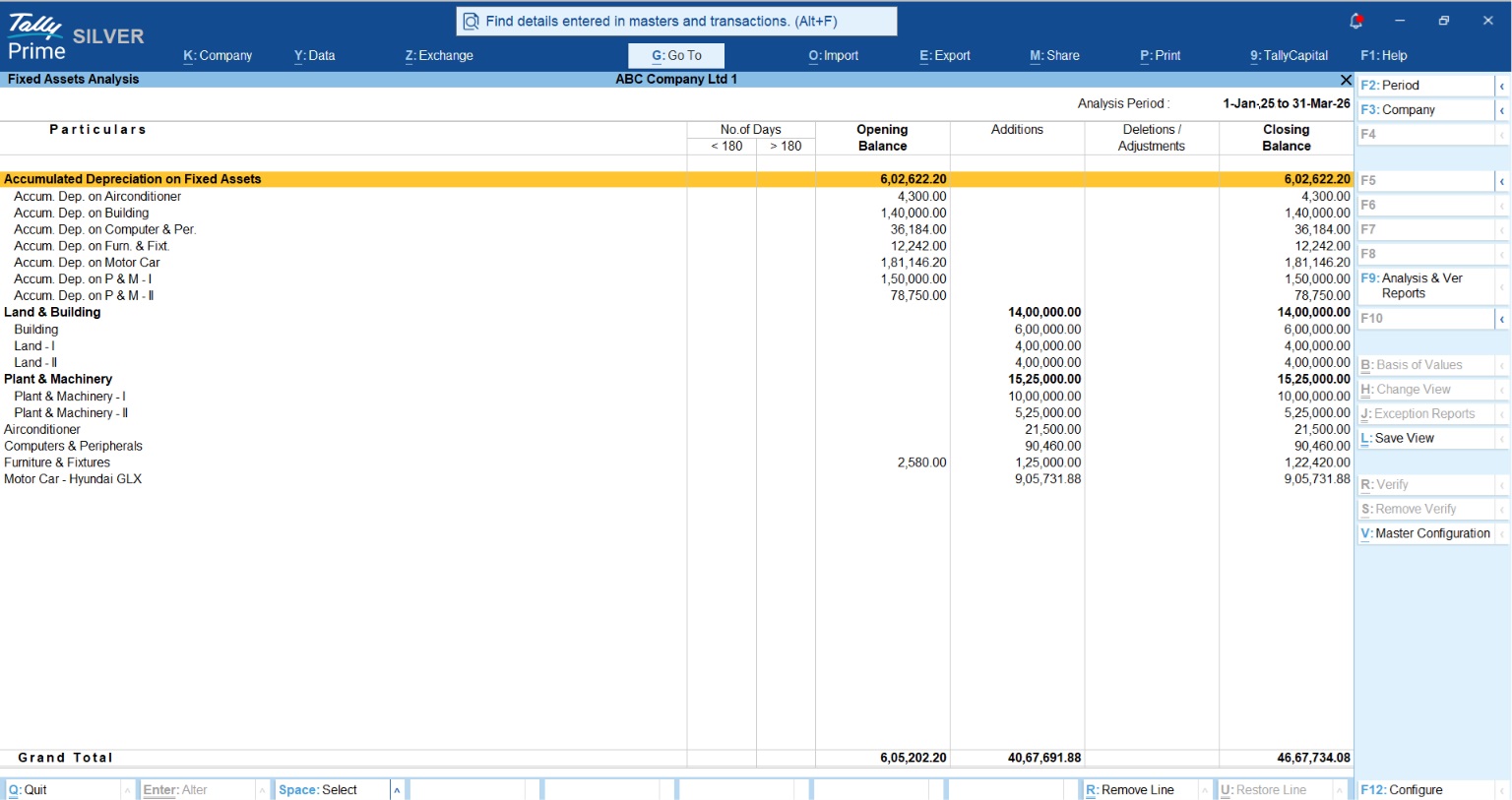

Why is a Fixed Asset Register (FAR) more than just a list?

A FAR isn’t just for your auditor; it’s a management dashboard that tells you exactly what you own and where your capital is locked up. A well-maintained FAR in TallyPrime offers:

- Asset accountability: Assign specific IDs, serial numbers, and custodians to every machine or laptop.

- Location tracking: Know exactly which branch or department houses specific equipment.

- Maintenance & warranty: Record AMC details, insurance expiry, and warranty periods to avoid out-of-pocket repair costs.

- Audit readiness: Instantly prove the physical existence of assets during statutory or tax audits.

Can TallyPrime calculate depreciation automatically?

Directly speaking: No, TallyPrime does not currently calculate depreciation percentages automatically at the ledger or item level. However, it provides a robust framework for recording these values manually through Journal Vouchers (F7).

Expert setup: The Cost Center Hierarchy To generate a professional "Depreciation Chart" that provides monthly breakups, do not just post a simple entry. Use this hierarchy:

- Create a cost category: Name it "Depreciation."

- Create cost centers: Under this category, create centers for each period (e.g., "April Depreciation," "May Depreciation").

- Recording the entry:

- Go to Gateway of Tally > Vouchers > F7 (Journal).

- Debit the "Depreciation" ledger (grouped under Indirect Expenses).

- Allocate the amount to the specific Cost Center (e.g., "April Depreciation").

- Credit the specific Fixed Asset ledger.

Pro-Tip from the Field: Avoid using one generic "Fixed Assets" ledger. In my experience, it's best to create separate ledgers for major asset classes, such as "Plant & Machinery" and "Computers", to mirror the "Block of Assets" required by the Income Tax Act. This makes your year-end tax planning significantly easier.

Also Read What is Depreciation? Meaning, Types & Methods Explained

Companies Act vs. Income Tax Act: How to balance both?

Indian businesses must navigate two different depreciation worlds. While the Companies Act 2013 focuses on the "useful life" of an asset to show a true and fair view of profits, the Income Tax Act (ITA) 1961 is designed for tax deductions.

|

Feature |

Income Tax Act (ITA) 1961 |

Companies Act 2013 |

|

Basis of Calculation |

Block of Assets (Grouped by class/rate) |

Individual Assets |

|

Method |

Written Down Value (WDV) is standard |

SLM or WDV (based on useful life) |

|

180-Day Rule |

50% depreciation if used for < 180 days |

Pro-rata based on actual days used |

|

Key Takeaway |

Purchase after Oct 3rd = 50% Depr. |

Depreciation starts from "Ready for Use" |

The "Block of Assets" Insight: For tax purposes, assets aren't sold individually; they are removed from a "block." This is vital because even if you sell an asset at a profit, you may not owe capital gains tax immediately if the remaining balance (WDV) of that block stays positive. This "tax shielding" is a critical strategic advantage for growing businesses.

What happens when you sell an asset?

The "moment of truth" for any asset is its disposal. To record this correctly, you must calculate the current book value (Original Cost minus Accumulated Depreciation).

When you sell an asset, remember:

- P&L computation: If you sell for more than the book value, it’s a profit; less is a loss.

- Sale proceeds & the block: Under the ITA, sale proceeds reduce the WDV of the entire block of assets.

- GST compliance: TallyPrime handles the GST implications on the sale of used assets, ensuring you don't fall foul of tax collectors.

- Automation hint: If you have high volumes of disposals, add-ons from TallyShop can instantly compute profit/loss and auto-generate the required journal entries, saving hours of manual reconciliation.

Real-world example: The "new machinery" scenario

Let’s look at a practical Straight-Line Method (SLM) calculation:

- Acquisition cost: ₹1,70,000

- Estimated residual value: ₹70,000

- Estimated useful life: 5 Years

- Depreciable amount: ₹1,00,000 (Cost - Residual)

Annual depreciation: ₹1,00,000 / 5 years = ₹20,000/year.

The Tally balance sheet impact (Year 1): At the end of the first year, your Balance Sheet will show:

- Machinery (cost): ₹1,70,000

- Less depreciation: ₹20,000

- Closing book value: ₹1,50,000

Handling assets "under construction" (CWIP)

If you are currently setting up a factory or installing machinery, those costs sit in Capital Work in Progress (CWIP).

- The Golden Rule: CWIP assets do not depreciate.

- The Trigger: Depreciation only begins when the asset is "Ready for Use", meaning it is in the location and condition necessary to operate as intended.

Pro-Tip: Don’t wait for a massive project to be 100% finished to start claiming benefits. If a specific "sub-asset" (like an individual machine in a new line) is ready for use, capitalize it immediately to begin claiming depreciation.

Conclusion & small business checklist

Digital tracking in TallyPrime beats manual spreadsheets every time because it links your physical assets directly to your financial truth.

Your 5-point actionable checklist:

- Verify opening balances: Ensure Tally’s fixed asset balances match your last audited return.

- Asset class mapping: Group ledgers into "Blocks" (Computers, Furniture, Plant) to simplify tax filing.

- Apply the 180-day rule: Identify any assets put to use after October 3rd to apply the 50% depreciation limit.

- Confirm CWIP status: Audit your CWIP ledger, if an asset is physically operational, move it to "Fixed Assets" now.

- Set up running balances: Use the configuration settings in Tally to view ledger reports with a running balance for easier month-end reviews.

"Depreciation isn't just an expense; it's a tax-saving tool that protects your capital for future growth."