Schedule III Division I of the Companies Act, 2013, is the statutory framework that governs how companies must present their financial statements. It prescribes the exact form and content of the balance sheet, the statement of profit and loss and the accompanying notes to accounts. Any company that does not qualify under Division II (Indian Accounting Standards) or Division III (non-banking financial companies following Ind AS) must follow Division I when preparing and filing its annual financial statements.

The Ministry of Corporate Affairs (MCA) introduced Schedule III to replace the older Schedule VI under the Companies Act, 1956, bringing greater consistency and comparability to corporate financial reporting across India.

What is Division I of Schedule III of the Companies Act, 2013?

Division I of Schedule III of the Companies Act, 2013, applies to companies that prepare financial statements under the Companies (Accounting Standards) Rules, 2006. It prescribes the format and disclosure requirements for presenting the balance sheet, the statement of profit and loss and the notes to the accounts, ensuring consistency and transparency in financial reporting.

Who must follow Division I?

Division I applies to all companies that prepare their financial statements under the Companies (Accounting Standards) Rules, 2006 and have not been notified to follow Ind AS. In practice, this covers most small and medium-sized companies that fall below the thresholds set for mandatory Ind AS adoption.

The following categories of entities are excluded from Division I, even if they do not follow Ind AS:

- Banking companies, which follow formats prescribed by the Reserve Bank of India (RBI) under the Banking Regulation Act, 1949.

- Insurance companies, which are governed by the Insurance Regulatory and Development Authority of India (IRDAI).

- Companies engaged in electricity generation or distribution, where sector-specific formats apply.

- Any other class of company for which a separate format has been specified under any other law.

What is the structure of financial statements under Division I

Division I mandates that every company present its financial statements in the following components:

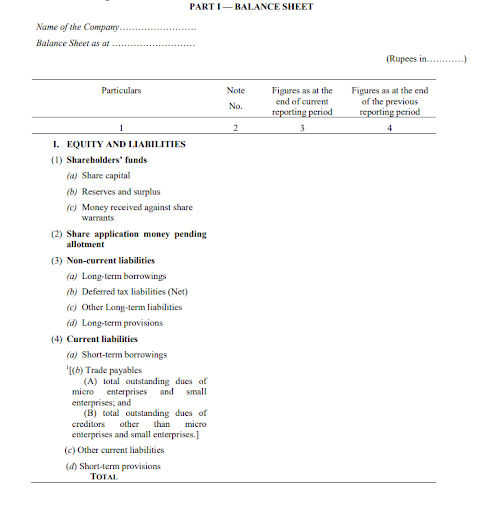

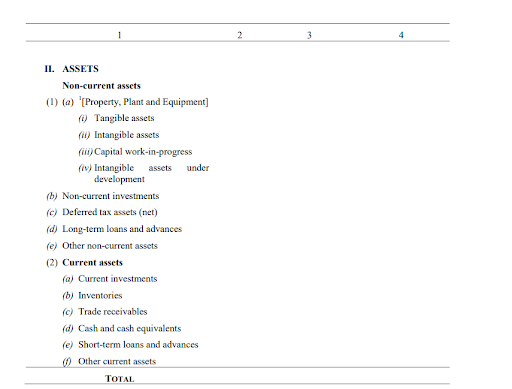

1. Balance sheet

The balance sheet must be presented in a vertical format, not the horizontal (T-account) format. It is split into two broad heads.

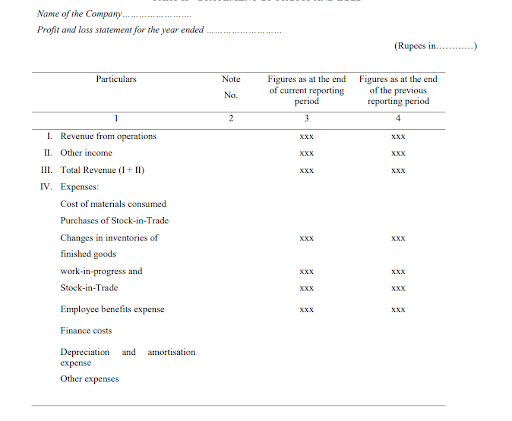

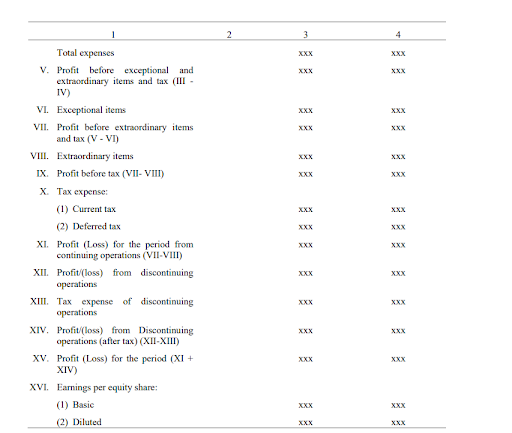

2. Statement of profit and loss

3. Notes to accounts

The notes to accounts are not optional. Division I specifies a set of mandatory disclosures that must accompany every financial statement. These include:

- Accounting policies adopted by the company.

- Details of share capital, including the rights, preferences and restrictions attached to each class.

- Reconciliation of the number of shares outstanding at the beginning and end of the reporting period.

- Details of long-term borrowings, including the terms of repayment and security.

- Maturity profile of loans and advances.

- Contingent liabilities and commitments not recognised in the balance sheet.

- Related-party transactions as required under the applicable accounting standard.

What are the additional requirements under Division I

Beyond the structural format, Division I imposes specific disclosure obligations that companies often overlook.

- Comparative figures: Every line item in the financial statements must show the corresponding figure for the immediately preceding financial year.

- Rounding off: Companies with a turnover of ₹100 crore or more must be rounded off to the nearest hundred, thousand, lakh, million or their decimal equivalents. Companies with a turnover of ₹1,000 crore or more must round off to the nearest lakh, million or crore, including their decimal values.

- Current and non-current classification: Assets and liabilities must be classified as current or non-current based on the business's operating cycle, which for most companies is 12 months.

- Going concern: If management is aware of material uncertainties that may cast significant doubt on the company’s ability to continue as a going concern, this must be disclosed.

Conclusion

Schedule III Division I is not a filing formality. It is the foundation of how a company communicates its financial position and performance to shareholders, lenders, regulators and other stakeholders. Getting the format, classification and disclosures right the first time avoids audit qualifications, RoC objections and the cost of restating financial statements.

Companies that use TallyPrime can generate compliant financial statements directly from their books, with the correct vertical balance sheet format, note references and comparative-year figures built into the reports.