Let me start with something nobody tells you at a pitch event.

I've sat across the table from founders who just closed their best month ever, record invoices raised, a new city launched, three senior hires onboarded and watched them struggle to explain why the bank account looked like it belonged to a struggling Kirana shop. Not because they lacked business. Because they had too much of it, too fast, with no cash to back it up.

That's the uncomfortable truth this piece is about.

Growth isn't the problem, unfunded growth is

Most startup advice is obsessed with growth. Grow faster. Hire aggressively. Capture market share before the competition does. And look, that instinct isn't wrong, exactly. But it's dangerously incomplete.

Here's what I've seen play out more times than I'd like to admit: a founder celebrates ₹80 lakh in monthly revenue, a team that's doubled in six months, and three new distribution channels. Meanwhile, I'm staring at a cash flow sheet showing ₹11 lakh in the bank, ₹23 lakh in unpaid salaries due Friday, and GST liability from two quarters ago still sitting unsettled.

On paper, the business is thriving. In the bank account, it's slowly suffocating.

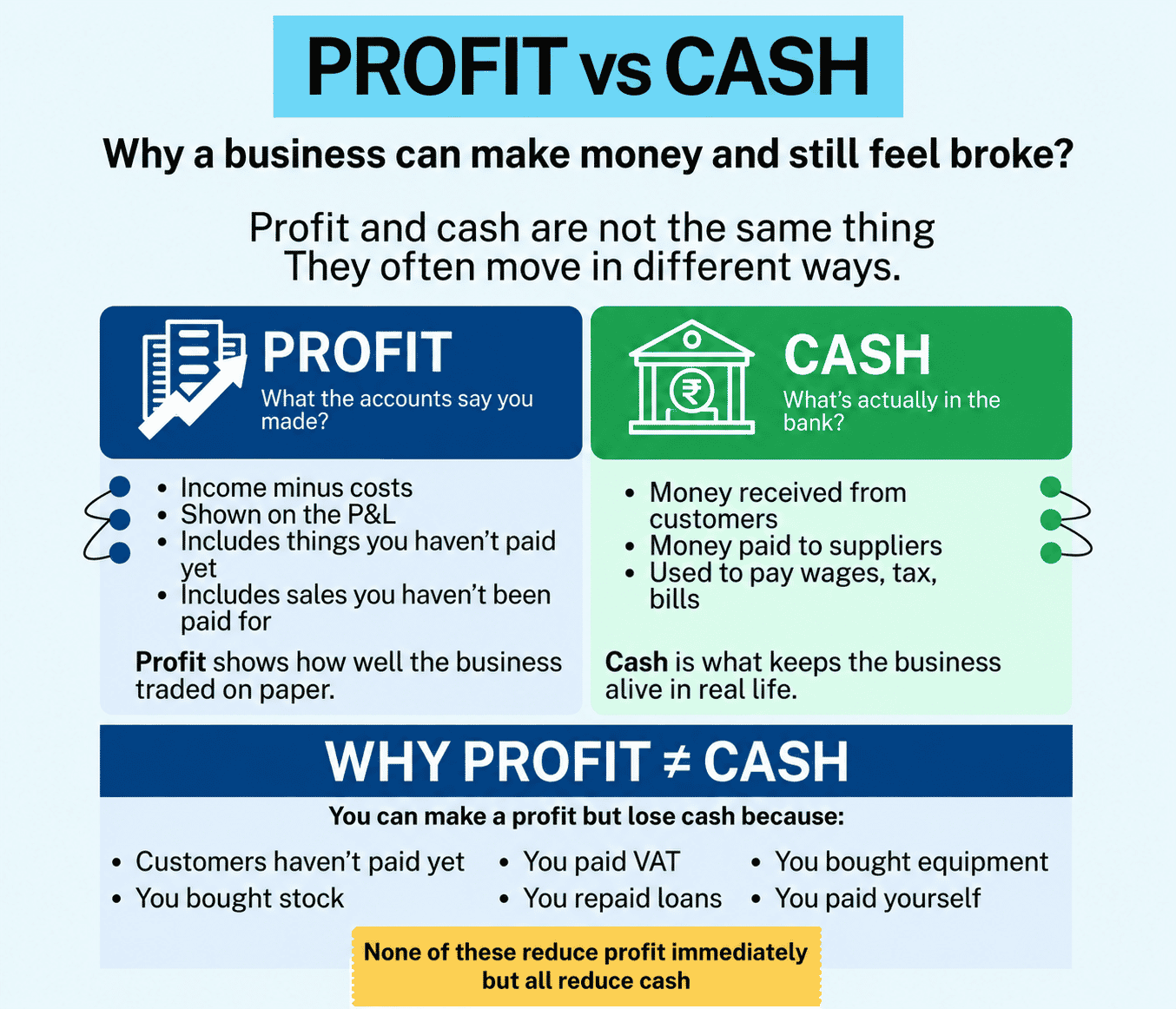

Revenue isn't cash. I know that sounds obvious when you read it, but founders stop believing it the moment growth starts looking exciting. A signed PO isn't cash. An investor's verbal commitment isn't cash. A ₹40 lakh invoice raised to a Fortune 500 company on net-90 terms is absolutely not cash, it's a three-month interest-free loan you just gave someone who didn't ask for it.

Cash is cash when it lands in your account. Everything else is hope.

The number that actually matters (And most founders ignore it)

There's a metric called the Cash Conversion Cycle (how long your money stays trapped in operations before returning as actual rupees). I cannot tell you how rarely I see early-stage founders track this. They track GMV, they track MoM growth, they'll proudly show you a DAU chart. But ask them how many days their working capital is locked up? Blank stare.

Here's a simple version of how it works in practice. Imagine you run a product business selling to retail chains.

|

Stage |

Days |

|

Pay the manufacturer |

Day 0-15 |

|

Inventory sitting in warehouse |

+30 days |

|

Goods dispatched to distributor |

Day 45 |

|

Payment finally received |

Day 90-105 |

That's a 75-90 day gap where your money is simply... gone. Working hard somewhere in the supply chain, sure. But not available to you.

Now triple your sales.

Congratulations, you've also tripled the cash you need to keep that cycle running. The founder says "we've grown 3x." I say "your working capital requirement just jumped from ₹9 lakh to ₹27 lakh, and we haven't talked about salaries yet."

Both statements are true. Only one determines whether you survive the next quarter.

Before agreeing to aggressive growth targets, do one thing: calculate the cash requirement per ₹1 lakh of sales. If it's ₹55,000–₹65,000 tied up for 60+ days, you don't have a growth plan, you have a funding gap dressed in optimistic clothing.

When the P&L looks great and you're still broke

I want to walk through something I've seen trip up even reasonably experienced founders.

A D2C brand I worked with was doing around ₹90 lakh monthly. Founders were thrilled. We sat down and built out the actual unit economics properly, not the back-of-napkin version, and this is roughly what we found:

|

Cost Element |

Per ₹1,000 Order |

|

Product (manufacturing) |

₹415 |

|

Packaging |

₹58 |

|

Shipping & last-mile |

₹94 |

|

Payment gateway fees |

₹24 |

|

Returns & damage buffer |

₹78 |

|

Performance marketing (blended) |

₹360 |

|

Total |

₹1,029 |

Every single order was losing ₹29 before you even count salaries, rent, software, or the founder's own time.

And here's the thing, they were about to double their ad spend because "the sales momentum was strong."

I've made similar mistakes in my own career, looking at top-line growth and convincing myself the underlying economics would improve at scale. Sometimes they do. Often they don't, especially when the growth is being bought through discounts and heavy marketing. Scaling a broken unit economics model doesn't fix it. It just makes the hole bigger, faster.

Why founders keep spending when they shouldn't

This part is less about numbers and more about psychology. And I think it matters.

When growth starts, something shifts emotionally. You stop evaluating decisions and start reacting to them. The investor wants to see expansion? Announce the second city. The competitor launched a new product line? Counter with something. The team is excited and working 14-hour days? Reward that with a bigger office.

Every one of those choices has a cash consequence. But they feel like leadership decisions in the moment, not financial ones. That's the trap.

I've watched founders take a ₹28 lakh monthly cost structure and scale it to ₹85 lakh in four months based on projections that never materialized. The projections weren't dishonest, they were just optimistic in the way all projections tend to be. The problem was that costs are immediate and certain while revenue is future and probabilistic. Rent doesn't wait for product-market fit. Vendors don't wait for your next funding round.

A disciplined operator knows when to pump the brakes. Not permanently, not out of fear, but long enough to make sure the foundation is solid before adding more floors.

The three gaps that quietly drain a growing business

In my experience, cash flow crises don't appear from nowhere. They build from one of three structural gaps:

The timing gap is the most common. You pay your suppliers in 30 days and collect from customers in 75-90 days. That difference, that 45-60 day float, is money you're effectively lending to the market. In B2B businesses especially, this can quietly become catastrophic as revenues scale.

The margin gap is sneakier. You're growing top-line numbers through discounts, aggressive CAC, free shipping, and loyalty programs. The revenue looks impressive but each unit is barely contributing. A 30% gross margin business that gives 22% discounts doesn't have a 8% margin anymore after returns, payment gateway, and variable logistics, it might have nothing at all.

The management gap is honestly the most dangerous, because it's invisible. The founder is running a ₹1.5 crore/month operation using the mental models of a ₹15 lakh/month business. No weekly cash review, no receivables ageing report, no purchase approval thresholds, no inventory movement analysis. It's not that the founder doesn't care, they're just too busy putting out fires to notice they're the one with the matches.

The B2B trap nobody warns you about

There's a particular kind of founder who feels safe because their clients are reputable companies. "We supply to major FMCG brand" or "Our anchor client is a large PSU." That sounds like stability. Often it's a slow drain.

Large Indian corporates, and this is a well-documented pattern, are notoriously slow payers to smaller vendors. You'll raise an invoice for ₹18 lakh and then spend the next three months navigating vendor registration portals, PO number corrections, GST reconciliation queries, finance team approvals, and payment cycle processing. Each step takes a week. Each delay is normal to them and existential to you.

Meanwhile you've already paid your team, your freelancers, your cloud subscriptions, and your advance tax.

In India, many MSMEs and startups aren't really in the business they think they're in. They're in the business of providing unsecured short-term credit to companies ten times their size. The solution isn't to avoid large clients, it's to negotiate terms properly before starting work.

Milestone billing, part advances, written payment schedules, and clear late payment clauses. These conversations feel awkward early in a client relationship. They feel a lot more awkward after you've been waiting 110 days for an invoice that was due in 45.

Discounting your way to disaster

Quick note on discounts, because I've seen this play out badly too many times.

A 20% discount on a product with 30% gross margin doesn't reduce your profit by 20%. It potentially wipes out the margin entirely and then some, once you factor in the variable costs that don't go away just because you dropped the price. You now need roughly three times the volume to earn the same gross profit as before.

When founders tell me "sales doubled after we ran that discount campaign," my first question is always: what happened to cash contribution? Usually the answer is uncomfortable. Revenue doubled. Cash position didn't improve. Sometimes it got worse.

What sensible scaling actually looks like

I want to be clear: I'm not arguing against growth. Fast growth, when it's properly funded and structurally sound, is exactly what you want. The goal isn't to slow down, it's to make sure the financial mechanics can support the speed.

Start with a 13-week rolling cash flow forecast. Not monthly, weekly. Track opening balance, confirmed inflows, committed outflows, salary dates, tax dues, vendor obligations, loan EMIs, and closing cash. Do this every single week. In a high-growth phase, a monthly review is too slow. Problems that show up in a monthly review are already emergencies. A weekly review gives you three to four weeks of advance warning.

Some practical gates worth setting:

- Don't hire for a new function until the gross profit from existing operations can cover that salary for at least six months.

- Don't launch city two until city one has been contribution-positive for at least a quarter.

- Don't increase ad spend unless your contribution margin per order is cleanly positive, not "expected to be positive next month."

- Don't stock inventory without evidence of actual sales velocity at that SKU level.

One founder I worked with ran every new service through three quick tests before launch: Could it be sold without deep discounting? Could it be delivered without disrupting what was already working? Could payment be collected within 30 days? If any answer was no, the idea went back into the backlog. Simple, almost blunt — but it kept the business from chasing shiny objects at the cost of operational cash.

When to slow down (Even when it hurts to say It)

Some signals that the brakes need touching, not permanently, but urgently:

Receivables growing faster than revenue is the clearest warning. It means you're booking sales but not collecting them. Vendor payments slipping every month is another, it means cash is being rationed. If salary planning depends on expected collections that haven't landed yet, you're already in fragile territory. Cash runway under three months with no clear bridge means stop, assess, and fix before pressing forward.

Slowing down isn't failure. A business that pauses to repair its financial structure can survive and accelerate again. A business that ignores these signals while appearing successful from the outside has a short window before the illusion becomes a crisis.

A final word on fundraising

Many founders believe that raising a round will fix cash flow problems. Sometimes it buys time. It rarely fixes the underlying issue.

If the unit economics are broken, capital gives you more runway to lose money. If collections are weak, capital masks poor credit management. If inventory decisions are driven by optimism rather than data, capital funds dead stock. I've seen well-funded startups fail precisely because the money made it easier to avoid confronting structural problems that a cash-constrained business would have been forced to solve early.

Raise from a position of understanding, not panic. Investors who've been around long enough can tell the difference between a founder who understands burn rate, cash conversion, and contribution margin and one who can quote user growth while having no idea what their working capital cycle looks like. The former earns trust. The latter raises a red flag, however good the deck looks.

Six things worth building into your process right now

- Weekly cash flow forecast, not monthly.

- Measure actual cash collected, not invoices raised.

- Calculate unit economics before deciding to scale anything.

- Set an inventory policy that's driven by sales velocity, not supplier minimums or optimism.

- Define customer credit limits and enforce them, even for clients that feel important.

- Keep three to six months of fixed costs as a reserve. If your monthly fixed base is ₹14 lakh, that means ₹42-84 lakh in cash that doesn't get touched for anything else.

Growth is genuinely exciting. I don't want to take that away. But the businesses I've seen survive long enough to become something meaningful are the ones where the founder understood that enthusiasm and cash discipline aren't opposites, they're partners. One gives you the vision.

The other keeps you alive long enough to execute it.