Time of supply refers to the time when output VAT is required to be paid. This is a mechanism which is used to determine the point in time when the tax liability will arise on a taxable transaction which a business is liable to pay. Time of supply is also called as Date of supply.

Just like how determining whether a supply is taxable or not, is important to determine the VAT applicability, similarly, determining the time of supply is very crucial for businesses to know the period in which the output VAT needs to be paid to the Government.

You might be wondering - why is the time of supply so crucial for business? As a business, I supply goods, collect VAT from my customer and I know the date on which I have collected VAT. Is this not sufficient to determine the tax period in which I have to pay the VAT to the government.

The answer is 'NO'.

Let us consider a scenario to understand why is Time of Supply or Date of supply crucial for businesses?

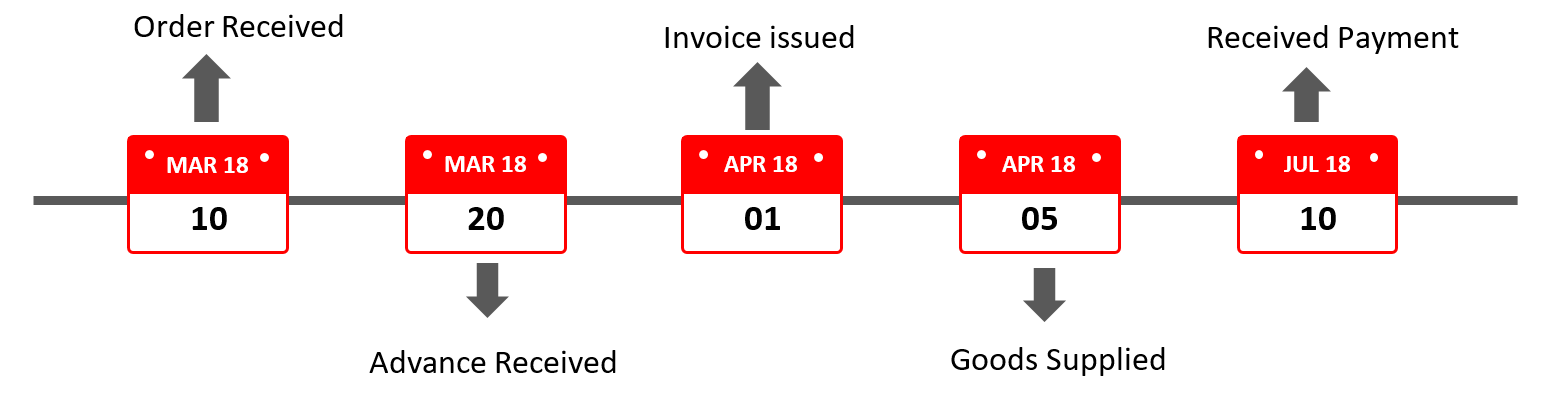

- 10th March, 2018 : Received an order from my customer to supply goods

- 20th March, 2018 : Confirmed the order and received advance payment (10% of supply value)

- 1st April, 2018 : Invoice is issued to the customer with details of supply and applicable VAT

- 5th April, 2018 : Goods are delivered to the customer

- 10th April, 2018 : Received full payment (remaining 90%) including VAT from the customer

Let us assume that you are required to file quarterly VAT returns i.e. Jan-Mar'18, Apr-Jun'18 and Jul-Sep'18.

If you closely look at the above illustration, a single transaction of supply consists of multiple dates spread across three VAT return periods.

Now, considering the above scenario, what will be the Time of supply?

Going with the plain understanding, you may think 10th July, 2018 as the time of supply since the full payment along with VAT is received only on 10th July, 2018. Another taxpayer may think, it should be the date of actual delivery of goods i.e. 5th April, 2018 and so on. This ambiguity does exist even in the case of supply of services too.

In order to remove the above ambiguity and to appoint one specific date for the taxpayer as well as for tax administration to quantify the amount of tax to be paid for the return period, the UAE VAT law is provisioned with the concept of 'Time of Supply'.

The concept of time of supply provides the manner of determining the date of supply by listing various dates related to supply of goods or services. The earliest occurrence of any such activities should be considered as the time of supply of goods or services on which tax will be due. Accordingly, the taxpayer need to report and remit VAT in the appropriate return period.

The time of supply in following business scenarios are discussed below:

-

- Time of supply for goods

- Time of supply for import of goods

- Time of supply in case of assembly or installation

- Time of supply in case of continuous supplies or progressive billing

- Time of supply for sale on approval or sale on return/consignment basis.

- Time of supply for voucher and vending machines

Time of Supply for goods

The following are the dates on which the liability of VAT will arise for supply of goods:

|

Supply of Goods |

|

|

Earliest of the following |

|

|

Date of Transfer of Goods |

The date on which goods were transferred, if such transfer was under the supervision of the supplier. If it is not under the supervision of a supplier, it will be the date on which the recipient of goods took possession of the goods. |

|

Date of Receipt of Payment |

This implies the date on which you have received payment for a taxable supply which includes advance receipt as well. |

|

Date of Tax Invoice |

Date on which the tax invoice is issued. The last date to issue tax is within 14 days from the date of supply. |

Time of supply for import of goods

|

Import of Goods |

|

The date on which the goods are imported under the Customs Legislation. |

Time of Supply for services

|

Supply of Services |

|

|

Earliest of the following |

|

|

Date of Completion of Services |

The date on which the services are completed. |

|

Date of Receipt of Payment |

This implies the date on which you have received payment for a taxable supply which includes advance receipt as well. |

|

Date of Tax Invoice |

Date on which the tax invoice is issued. The last date to issue tax is within 14 days from the date of supply. |

Time of supply in case of Assembly or Installation

|

Assembly or Installation |

|

Date on which the assembly or installation is completed. |

Time of supply in case of Continuous Supplies or Progressive Billing

|

Earliest of the following |

|

Date of Tax Invoice |

|

The date of payment is due as shown on the Tax Invoice |

|

The date of receipt of payment |

Note: This is applicable only if periodic payments or consecutive invoices does not exceed one year from the date of the provision of such goods and services.

Time of supply for sale on approval or sale on return/consignment basis.

|

Sale on Approval/ Sale on return/consignment basis |

|

Earliest of the following |

|

Date on which supply of goods was accepted by the recipient. |

|

Lapse of 12 months from the date of delivery by the supplier or goods placed at the disposal of the recipient. |

Time of Supply in case of Deemed Supplies

|

Deemed Supplies |

|

Earliest of the following |

|

Date when it is deemed to be have been supplied |

|

Date of disposal |

|

Date of change in usage |

Time of supply for voucher and vending machines

|

Time of supply for voucher and vending machines |

|

|

Earliest of the following |

|

|

Voucher |

Date of issue or supply (redemption of voucher) thereafter |

|

Vending Machines |

Date on which funds are collected from the machine |

The concept of time of supply is very crucial for businesses in determining the date on which the output VAT is due for supply and it subsequently helps in payment of VAT for the respective VAT return period. Any discrepancies in determining the time of supply will have significant impact on the cash outflow of the business. Wrong determination of time of supply will either lead to delay in paying the tax which will attract a penalty or you may end up, in early payment of tax which will impact your cash outflow.