If you’re pricing a product and want to know exactly what each extra unit will cost you, you’d want to use variable costing. It assigns only variable production costs (that’s your direct materials, direct labour and variable overhead) to your products, leaving fixed costs out of the equation entirely.

The result is a clearer read on how your costs and profits change with output. It also highlights contribution margins and supports practical decisions on pricing, special orders and cost control.

What are variable costs?

Variable costs are expenses that change in direct proportion to production or service volume. Put simply, they rise when production goes up and fall when it slows down. In contrast, fixed costs remain unchanged, regardless of activity.

Common examples include:

- raw materials

- direct labour wages

- sales commissions

- machine-linked utility costs

For example: A bakery producing more cakes needs more flour and eggs, so those ingredient costs move with output, while the monthly lease stays the same no matter how many cakes go out the door.

This is the basis of variable costing (also called direct costing): it separates these output-driven costs from fixed costs and treats them differently in decision-making. Mixing the two can lead you to the wrong conclusion.

How to calculate variable costing (with practical examples)

Variable costing is calculated by isolating all variable production costs and expressing them on a per-unit and total basis to understand cost behaviour and profitability.

Variable Cost per Unit = (Direct Labour Cost + Direct Raw Material Cost + Variable Manufacturing Overhead) ÷ Number of Units Produced

Total Variable Cost = Total Output Quantity × Variable Cost per Unit

To apply these formulas correctly, follow these steps:

- Start by identifying direct labour costs, which are wages directly attributable to production, based on pay rate, skill level and hours worked. In some businesses, this may be fixed or semi-variable depending on employment arrangements.

- Next, determine the direct raw material cost by identifying the materials used per unit and their costs.

- Then isolate the variable portion of manufacturing overheads, such as power consumption or packaging, which increase as output rises.

After identifying these components, note the total number of units produced during the period. Add the three variable cost elements and divide by total units to arrive at the variable cost per unit.

Now, let's look at some practical examples:

Example 1: Furniture manufacturer

A small furniture manufacturer produces wooden chairs and wants to determine its variable cost per unit before setting a selling price. The management accountant provides the following data:

- Raw material per chair (wood, screws, finishing): ₹1,200

- Direct labour per chair: ₹600

- Variable manufacturing overhead per chair (power, consumables): ₹400

- Fixed costs for the period (factory rent, depreciation): ₹15,00,000

Under variable costing, factory rent and depreciation are treated as period expenses because they are incurred regardless of output, so including them in per-unit cost would distort the incremental cost of producing one more chair.

Therefore:

Variable Cost per Unit = ₹1,200 + ₹600 + ₹400 = ₹2,200 per chair

This means each additional chair incurs variable expenses of ₹ 2,200. Any selling price above ₹2,200 helps cover fixed costs and profit, while a price below this level reduces the contribution margin and is typically not sustainable over time.

Example 2: Plastic packaging manufacturer

A plastic packaging manufacturer produces 15,00,000 containers annually and needs to evaluate a bulk special order. The income statement shows the following costs:

|

Cost Item |

Amount (₹) |

|

Raw materials |

18,00,000 |

|

Labour cost |

9,00,000 |

|

Machinery depreciation (fixed) |

6,00,000 |

|

Factory insurance (fixed) |

3,00,000 |

|

Equipment maintenance (fixed) |

4,50,000 |

|

Utilities (fixed overhead) |

2,40,000 |

|

Utilities (variable overhead) |

9,00,000 |

|

Total manufacturing cost |

51,90,000 |

Not all costs are relevant for this decision. Fixed costs like depreciation, insurance, maintenance and fixed utilities remain unchanged whether the order is accepted or not. The focus is on the cost of producing additional units.

Variable Cost per Unit = (₹18,00,000 + ₹9,00,000 + ₹9,00,000) ÷ 15,00,000 = ₹2.40 per container

The incremental cost of producing one more container is ₹2.40. If the offer price is ₹2.80, the contribution per unit is ₹0.40.

Assume the company receives a special order for 5,00,000 containers at an offer price of ₹2.80 per container.

Total contribution = ₹0.40 × 5,00,000 = ₹2,00,000

If the company has spare capacity and no additional fixed costs arise, accepting the order adds ₹2,00,000 directly to profit. This example shows how variable costing focuses only on costs that change with production, leading to more accurate and practical decisions.

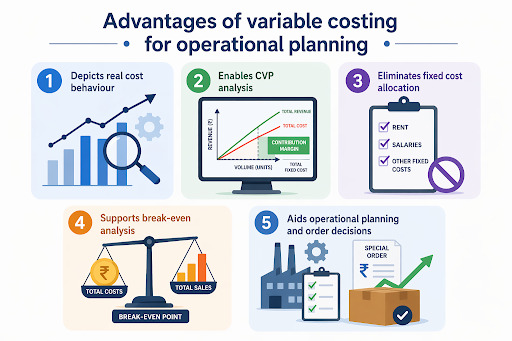

What are the advantages of variable costing for operational planning?

(This image was created using AI)

Variable costing may not be used in external financial reporting, but it is highly useful for internal decision-making. Managers rely on it for the following reasons:

- Depicts real cost behaviour: By focusing only on costs that change with production volume, it provides a clear view of how costs move as output rises or falls.

- Enables CVP analysis: Cost-Volume-Profit (CVP) analysis examines how changes in costs and volume affect profit. Variable costing simplifies this by clearly showing contribution margin, helping businesses identify profitable products and allocate resources effectively.

- Eliminates fixed-cost allocation: Allocating fixed costs such as rent or salaries across units can be subjective and time-consuming. Variable costing removes this complexity, keeping the process straightforward.

- Supports break-even analysis: It helps calculate the break-even point, the minimum sales volume required to cover total costs, making it a practical planning tool.

- Aids operational planning and order decisions: It supports production planning and evaluation of special orders. If the price exceeds the contribution margin, the order adds to profit, a conclusion that variable costing makes easier to assess.

Can variable costing be used for external financial reporting?

Variable costing is useful for internal decision-making but is not permitted for external financial reporting, as accounting standards require absorption costing.

Standards such as IFRS and, in India, Ind AS mandate absorption costing. Under this method, all manufacturing costs, including fixed costs like factory rent, factory salaries and depreciation on production equipment, are included in inventory.

This ensures expenses are recognised in the same period as the revenue they generate, in line with the matching principle.

Variable costing includes only variable production costs and treats fixed manufacturing costs as period expenses, resulting in different profit and inventory figures. For external users like investors, lenders and regulators, financial statements must be consistent and comparable. Allowing different costing methods would reduce reliability, which is why variable costing is used only for internal purposes.

Conclusion

Variable costing may not appear in financial statements, but it remains one of the most practical tools for day-to-day business decisions. By focusing only on costs that change with output, it shows exactly what it takes to produce one more unit and whether that decision adds value. This clarity makes pricing, break-even analysis and special-order evaluation far more reliable.

For businesses that want accurate cost insights without unnecessary complexity, tools like TallyPrime help streamline cost tracking, accounting and reporting.

Backed by a 40-year legacy and trusted by over 2.7 million businesses across India, it enables faster, better-informed decisions that support sustainable growth.