MACRS, which stands for Modified Accelerated Cost Recovery System, is the US federal tax depreciation system used to recover the cost of eligible business assets over a specified recovery period through annual tax deductions. Under MACRS, assets are placed into sections defined by the Internal Revenue Service (IRS), like 3-year, 5-year, or 7-year classes, reflecting how fast an asset's cost is deducted over time. Businesses can usually claim bigger depreciation deductions in the first few years. This system is commonly used for equipment, machinery, vehicles, furniture and certain buildings placed in service for business use.

What is MACRS Depreciation?

MACRS depreciation is the depreciation framework used in the US for federal income tax purposes. It was introduced under the Tax Reform Act of 1986 and replaced the earlier Accelerated Cost Recovery System (ACRS). The system sets standard recovery periods and approved calculation methods for different types of assets, making tax depreciation more structured and consistent.

Businesses use MACRS when claiming deductions on assets placed in service for business use, such as equipment, furniture, vehicles, and buildings. Depending on the asset category, the IRS allows deductions over a fixed schedule rather than businesses guessing how long the asset will last. This, in turn, makes MACRS an important tool for tax planning, compliance, and capital investment decisions.

How does MACRS Depreciation Work?

MACRS depreciation applies in the US for federal tax purposes when businesses buy eligible assets for business use. It works in the following steps:

- Identify the asset: Confirm that the asset is eligible for depreciation and used for business purposes.

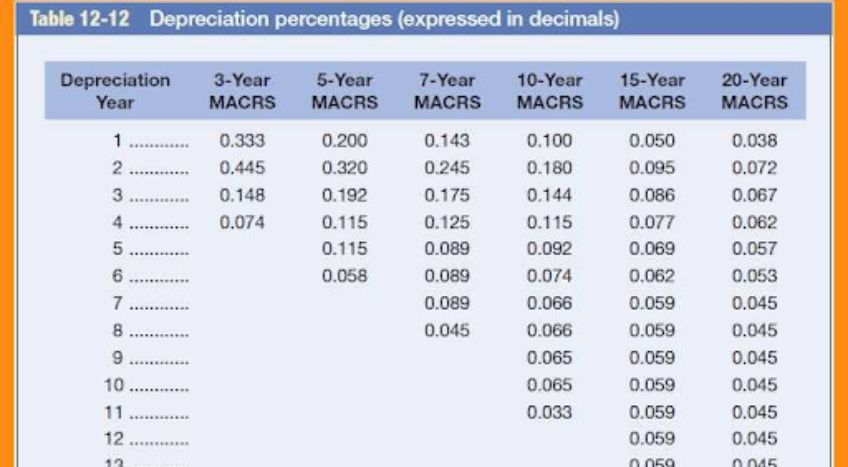

- Assign the asset class: Place the asset into the correct IRS category, such as 5-year, 7-year, or 39-year property.

- Choose the method: Use the allowed depreciation method, such as accelerated or straight-line.

- Apply the convention: Follow IRS timing rules for the first and last year of deduction.

- Claim yearly deductions: Deduct the allowed amount each year until the asset’s cost is fully recovered.

Factors that Determine MACRS Depreciation

The amount of depreciation claimed under MACRS depends on several important factors.

- Type of asset: Different assets, such as computers, vehicles, furniture, or buildings, are assigned different recovery periods.

- Purchase cost: The total cost of the asset, including eligible expenses, forms the basis for depreciation.

- Date placed in service: Depreciation begins when the asset is ready and used for business, not just when it is purchased.

- Recovery period: The IRS sets the number of years over which the asset’s cost can be recovered.

- Depreciation method: The deduction may be calculated using accelerated or straight-line methods.

- Convention used: IRS timing rules affect first-year and last-year deductions.

- Business-use percentage: If an asset is used partly for personal use, only the business portion may qualify.

How to Calculate MACRS Depreciation

The amount of depreciation claimed under MACRS determines how much deduction a business can take each year and how long the asset will be depreciated.

Formula

Depreciation in 1st Year

Depreciation = Cost × (1 ÷ Useful Life) × Depreciation Method × Depreciation Convention

Depreciation in Subsequent Years

Depreciation = (Cost – Previous Years’ Depreciation) × (1 ÷ Recovery Period) × Depreciation Method

Calculation Example

Suppose a business buys a computer for $10,000. The computer is classified as 5-year property under MACRS and uses the 200% declining balance method with the half-year convention.

First-Year Calculation

Depreciation = Cost × (1 ÷ Useful Life) × Depreciation Method × Convention

Depreciation = 10,000 × (1 ÷ 5) × 2 × 0.5

Depreciation = $2,000

Second-Year Calculation

Remaining Value = 10,000 – 2,000 = $8,000

Depreciation = Remaining Value × (1 ÷ Recovery Period) × Depreciation Method

Depreciation = 8,000 × (1 ÷ 5) × 2

Depreciation = $3,200

Remaining Value after Year 2 = 10,000 – (2000 + 3200)

= $4,800

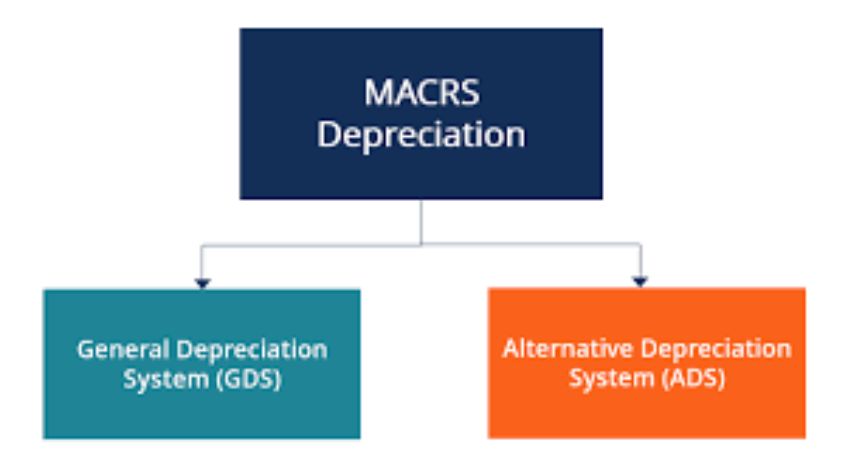

Depreciation Systems in MACRS

MACRS uses two main depreciation systems: the General Depreciation System (GDS) and the Alternative Depreciation System (ADS).

General Depreciation System (GDS)

GDS is the standard system used by most businesses. It generally allows faster cost recovery and higher deductions in the earlier years of an asset’s life. Because of this, it is the most commonly used option under MACRS.

Property classification under GDS

|

Property Class |

Examples |

|

3-year property |

Certain tools, tractors, racehorses |

|

5-year property |

Computers, office equipment, vehicles |

|

7-year property |

Office furniture, fixtures, machinery |

|

10-year property |

Certain boats, agricultural assets |

|

15-year property |

Land improvements, roads, fencing |

|

20-year property |

Farm buildings, utility property |

|

27.5-year property |

Residential rental property |

|

39-year property |

Non-residential commercial buildings |

The methods used here include 200% declining balance, 150% declining balance, or straight-line. These methods decide how the asset’s cost is spread over time.

- 200% declining balance method: An accelerated method that gives larger depreciation deductions in the early years and smaller deductions later. It allows faster cost recovery.

- 150% declining balance method: Similar to the 200% method but with a slower rate of acceleration. Deductions are higher in the beginning, but less aggressive than the 200% method.

- Straight-line method: Spreads the asset’s cost evenly over its recovery period, resulting in the same depreciation amount each year.

Alternative Depreciation System (ADS)

ADS is a slower depreciation system under MACRS. It generally uses longer recovery periods and the straight-line method, which spreads deductions more evenly over time. This usually results in lower annual deductions compared with GDS.

When is ADS Applicable?

ADS may be required when property is used mainly outside the United States, as different tax rules apply to foreign-use assets. It can also apply to certain tax-exempt use property or assets financed with tax-exempt bonds.

Some farming businesses may need to use ADS depending on the elections or provisions they choose under tax law. In other cases, a business may voluntarily elect ADS to maintain consistency in reporting or align tax treatment across assets.

The method used is straight-line only.

MACRS Depreciation vs Depletion: Key Differences

MACRS depreciation and depletion are both methods used to recover costs for tax purposes, but they apply to different types of assets. MACRS is used for physical business assets, while depletion is used for natural resources that are extracted or consumed over time.

|

Basis |

MACRS Depreciation |

Depletion |

|

Meaning |

Tax method to recover the cost of business assets over time |

Method to recover the cost of natural resources as they are used |

|

Applies To |

Machinery, vehicles, furniture, equipment, buildings |

Oil, gas, minerals, timber, coal, and similar resources |

|

Asset Type |

Tangible depreciable assets |

Wasting natural resource assets |

|

Basis of Deduction |

Recovery period set by IRS |

Quantity extracted or percentage of income from the resource |

|

Common Methods |

200% declining balance, 150% declining balance, straight-line |

Cost depletion and percentage depletion |

|

Deduction Pattern |

Fixed schedule over set years |

Based on production or allowed percentage |

|

Main Purpose |

Recover the purchase cost of the business property |

Recover investment in natural resource reserves |

MACRS Depreciation and Revaluation Methods

MACRS depreciation and revaluation both relate to asset values, but they are used for different purposes. MACRS is a tax method, while revaluation is an accounting method.

MACRS does not use revaluation to adjust an asset to market value. Instead, it follows fixed tax depreciation methods to calculate yearly deductions and may switch to the straight-line method when it gives a better deduction.

- Meaning: MACRS depreciation helps businesses recover the cost of assets through yearly tax deductions. Revaluation updates the recorded value of an asset to match its current market value.

- Purpose: MACRS is used to reduce taxable income over time. Revaluation is used to show a more accurate asset value in financial statements.

- Application: MACRS applies to U.S. federal tax reporting. Revaluation is commonly used under accounting standards such as IFRS.

- Value Treatment: Under MACRS, asset value decreases over time. Under revaluation, asset value can increase or decrease based on market conditions.

Conclusion

MACRS helps businesses recover asset costs through structured tax deductions, while depletion and revaluation apply in different situations, such as natural resources and fair-value accounting. Understanding these methods supports better compliance, tax planning, and financial reporting. For businesses that want to simplify fixed asset tracking, depreciation calculations, and accounting records, TallyPrime offers integrated solutions to manage assets efficiently and maintain accurate books with ease.