Understanding cash flow vs. profitability — and avoiding dangerous conclusions

When a “profitable” business asked for emergency funding

I was reviewing numbers with a business owner after closing monthly accounts.

The P&L looked healthy. Margins were decent. The bottom line showed profit.

Then he said something that stopped the discussion:

“We’re profitable on paper, but I’m struggling to pay salaries this month.”

This wasn’t a rare case.

It’s one of the most common — and most misunderstood — financial realities in business.

Profit does not mean cash.

And confusing the two quietly hurts otherwise good businesses.

Profit vs cash: The difference most businesses learn too late

Let’s keep this simple.

Profit

- Shown in the Profit & Loss statement

- Based on revenue earned and expenses incurred

- Includes credit sales and non-cash expenses

Cash

- What’s actually available in the bank or cash box

- Determined by when money comes in and goes out

- Dictates whether you can pay people, vendors, and taxes

A business can:

- Show profit but have no cash

- Have cash today but be unprofitable

The danger lies in assuming profit equals financial safety.

The common misconceptions that create cash stress

1. “Sales have increased, so cash will improve”

Not if:

- Sales are on long credit terms

- Customers delay payments

- Receivables pile up

Revenue is recorded when invoiced — cash comes only when collected.

2. “We’re profitable, so we can expand”

Expansion needs cash:

- More inventory

- Higher receivables

- Advance payments

Many profitable businesses fail during growth because working capital wasn’t planned.

3. “Expenses are under control, so we’re safe”

Some costs don’t hit cash immediately:

- Depreciation

- Provisions

- Accrued expenses

They reduce profit but don’t use cash — which can mask future cash outflows.

4. “GST, TDS, and Advance Tax will manage themselves”

Taxes are often:

- Collected today

- Paid later

Until payment is due, the cash feels available —

but when deadlines hit, businesses scramble.

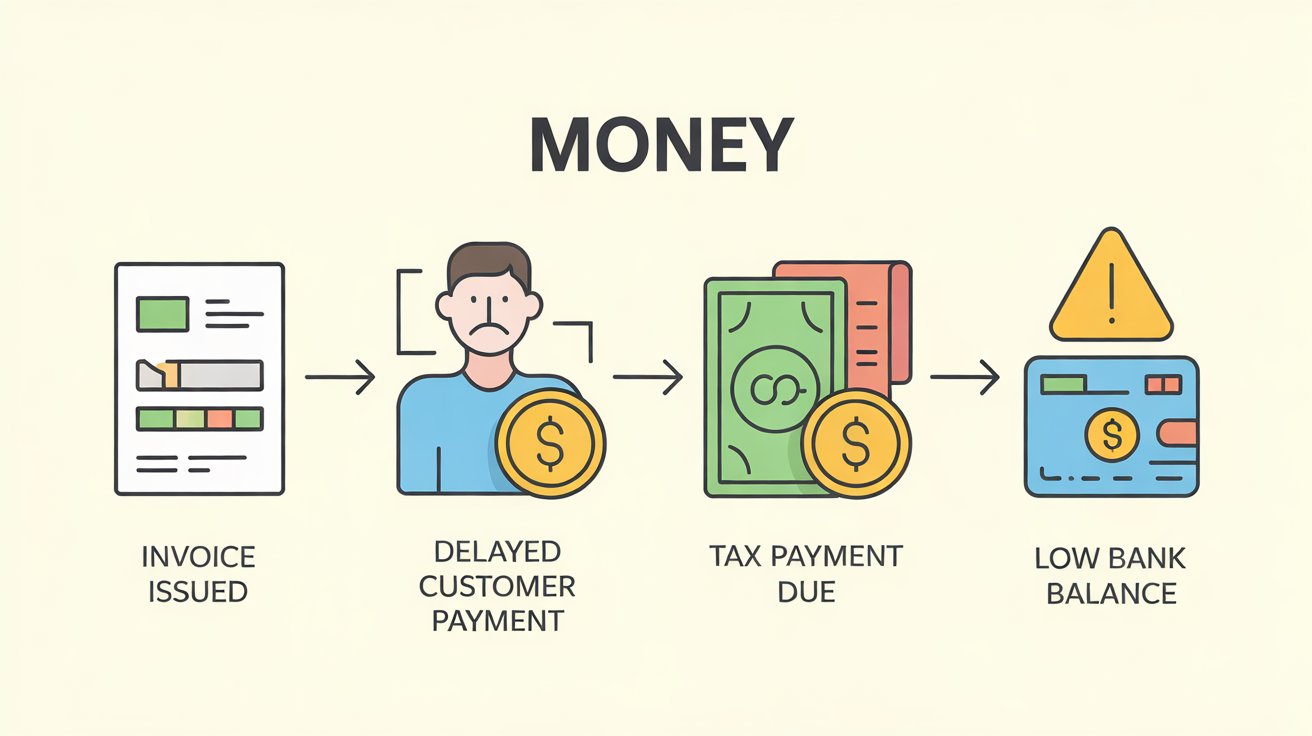

A real-world example I see often

A trading business shows:

- ₹1 crore in monthly sales

- 8% net profit

But:

- Customers pay after 90 days

- Inventory is purchased upfront

- GST is payable before collections

Result?

- Strong profits

- Constant overdraft usage

- Stress during tax payment dates

This is not bad management — it’s misunderstanding cash flow.

Why cash flow needs separate attention

From a CFO’s perspective, cash flow answers three critical questions:

- Can we survive the next 90 days?

- Can we meet statutory obligations on time?

- Can we grow without borrowing excessively?

That’s why smart finance teams:

- Track receivables ageing closely

- Monitor payables timing

- Forecast cash, not just profit

Practical steps to avoid the profit–cash trap

Here’s what actually works in real businesses:

Track cash separately

Don’t rely only on P&L. Review:

- Bank balances

- Cash flow statements

- Weekly inflow–outflow summaries

Shorten collection cycles

- Clear credit policies

- Regular follow-ups

- Early payment incentives

Plan tax cash outflows

Set aside GST, TDS, and advance tax amounts — mentally and in accounts.

Use systems that show the full picture

Accounting platforms like TallyPrime help businesses see:

- Profitability

- Outstanding receivables

- Payables

- Cash and bank positions

Together — not in isolation.

A CFO’s closing thought

I’ve learned this over years of reviews and audits:

Profit tells you how well the business performed.

Cash tells you whether the business will survive.

Strong businesses respect both.

If decisions are made only on profit numbers, cash problems will follow — quietly, steadily, and painfully.

Understanding the difference early is not accounting knowledge.

It’s business wisdom.